|

17th May 1998 |

Front Page| |

||||||||||||||||||||||||

Contents

|

||||||||||||||||||||||||||

|

All round aid cuts affect Lanka tooBy Feizal SamathSri Lanka is unlikely to get more than US$ 700 million in concessional foreign aid at this month's Paris aid group meeting - much below the US$ 850 million received last year - because of the global environment where aid flows to poor countries are easing, a World Bank official said. "I believe that even if the Sri Lanka delegation does extremely well (in making a pitch for sufficient aid) at the Paris meeting, there is not going to be much of a chance for overall pledges to be above US$ 700 million," Roberto Bentjerodt, World Bank representative in Sri Lanka, told "The Sunday Times" Business. But he noted that the US$ 700 million-plus expected this year would represent a substantial commitment in the context of shrinking aid flows. Donors and foreign agencies providing aid to Sri Lanka meet in Paris for two days later this month for the annual aid-Sri Lanka parley. The government has also expressed similar concerns that aid flows this year may not be in keeping with previous trends in view of a "shrinking aid pie". Bentjerodt said one of his concerns was that the Sri Lankan business community may see the lower levels of aid as a reflection of the level of confidence by donors helping the country. "This (low amount) by no means should be seen as a lack of confidence by the donor community in Sri Lanka and her economic and social policies. It is just a fact that the pool of aid resources that is available is shrinking very fast," he said. According to World Bank figures, concessional aid - which is what Sri Lanka gets and which is a fraction of total aid flows - to the poorest countries fell to US$ 37 billion last year from US$ 40 billion in 1996. Official development finance in terms of net flows fell to US$ 44.2 billion in 1997 from US$ 56.4 billion in 1990, says the World Bank's Global Finance Report for 1998 released last month. Financial experts say such figures indicate that overall aid volumes in the world have been cut by half, if one is to take into account the purchasing power of the dollar now and eight years ago. The World Bank representative in an interview praised Sri Lanka's economic achievements and social development strategies, and explained in detail the background scenario with regard to the global availability of aid. He said that worldwide, donor countries were facing severe fiscal problems and donors in East Asia, on top of this, have been confronted with the financial and foreign currency crisis. Large donors including Japan, which is less affected by the East Asian crisis, were re-channeling aid to help their neighbours desperately in need of emergency assistance. This then resulted in difficulties in maintaining even levels of aid that were close to pledges made in the past to poor countries. Bentjerodt said Sri Lanka would continue to enjoy high levels of aid but from a smaller pool of resources. "Sri Lanka in the past has received special treatment from donors in the past for a variety of reasons including significant achievements in human (social) development and sympathy for the problems faced by the country," he said. He said that Sri Lanka will not be affected by the declining aid levels because foreign aid flows financed a very small share of investments in the country. "Overall - in the '90s - the quality of economic policy has improved and that is reflected in the country's self-reliance," he added. The World Bank's favourable view of economic policy and country achievements is also supported by the Central Bank in its 1997 annual report which goes on to illustrate the high rate of economic growth at 6.4 percent and other positive developments in agriculture and other sectors. But is this an illusion - masking the real problems in the Sri Lankan economy,? as succinctly put by Professor Sirisena Tillakeratne, an economics teacher and Chairman of the University Grants Commission. Prof. Tillakeratne, on a panel that last week discussed the Central Bank report and the state of the economy, present and future, said the Central Bank indicators painted a positive picture of the economy but he noted that there were several hidden negative factors that needed to be addressed. Among them were agriculture which, he observed, was in bad shape with some recent studies showing that the once-stable rural economy was slowly becoming dependent on Middle East remittances - the families of farmers working abroad and repatriating their wages. Central Bank officials however countered Tillakeratne's arguments. Yet the Central Bank symposium left many participants reflecting on the good professor's views and wondering whether there were hidden issues of a serious nature in the economy.

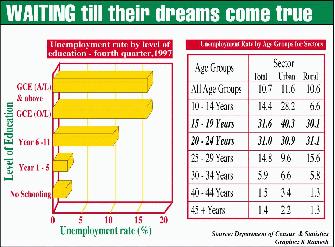

Jobless young look for jobs that aren't thereBy Mel GunasekeraDespite 1997's economy generating about 75,000 additional jobs, youth unemployment remains high. Most educated unemployed youth crave for high profile jobs and are willing to wait until they get the 'ideal job', a top economist said. Unemployment rate is highest among youth between 15-29 years, the Department of Census and Statistics reports. During the third quarter of 1997, 0.6 per cent of job aspirants desired agriculture based occupations while about 33 per cent preferred 'white collar jobs'. Unemployment decreased from 11.4 per cent in 1996 to 10.4 per cent in 1997. The expansion of informal sector activities, creation of new job opportunities in the fields of computer, electronic media, financial services and a continuation of high migration for foreign employment, appear to be the major contributory factors to the decline in unemployment, the Central Bank 1997 Report states.

There were a number of reasons why the numbers were so high. To begin with, the rate of job creation is much lower than those who come in, the economist said. Too high expectations is another factor. Workers are more educated and they aspire for better status, well paid jobs. Circumstances do not make them seek for lower employment. "There is no impetus to push them down and the doting parents continue to support them till they secure their dream job. Their job ideal is what the parents, society and peers desire for them," she said. Despite heavy bureaucracy and general lethargy, the state sector remains attractive, because it offers permanent stability. However, public sector employment declined in 1997, solely due to a 24 per cent decline in semi-government sector employment. The transfer of 22 plantation companies in 1997 to the private sector under long-term lease agreements, coupled with the public sector reform policies was also attributed to the general decline. However, employment in the government sector, including the central government, provincial councils and local authourities registered a 1 per cent increase in 1997. The increase was largely reflected in the categories of clerical and related workers, administrative and managerial workers. "Political imperatives is another factor," she said. Successive governments tend to absorb unemployed youth in an ad hoc manner (like the Samurdhi programme which absorbed 36,000 youth). There is also a high reservation wage (what the unemployed have to forgo if they get a job). In this instance, family support is crucial. Remittances from Middle East, the Samurdhi hand-outs, patron-client networks (mudalalis, politicians supporting families), family members joining the forces, illegal activities like timber felling, illicit distilling and gem mining keep these people going. "Basically, by and large, these people seem to get by" she said. There is also a mismatch of skills. The skills demanded by the local industry are not available. Our economic scenario is not too sophisticated. Most domestic industries are low skilled operations which require GCE O/L. The demand is only for particular types of skills like computer, electrical engineering, but management skills are still lacking. "Even if you provide jobs for these particular skills, unemployment levels will not go down as they are not that significant," she said. "However, no qualitative assessment on this particular issue has been done yet. They remain a hypothesis. None of these reasons are mutually exclusive, but they all play an important role," she added. The major challenge ahead is to reduce unemployment by reformulating the education system so as to match the growing labour force to the changing needs of the economy, particularly the needs of the private sector, President, Federation of Chambers of Commerce and Industry Sri Lanka (FCCISL), Patrick Amarasinghe said. The FCCISL is in the process of training graduates through the Tharuna Aruna Programme. The programme which commenced last year, is training 3,000 unemployed graduates. Nearly 80 per cent of those selected were arts graduates. Todate, around 1,200 have been placed in various organisations, both private and non-governmental throughout the country.

Question mark hangs over Airbus 20% discountBy Ruvini JayasingheFuelled by fierce competition, the Airbus vs. Boeing price war and their generous shower of discounts have put a huge question mark on Air Lanka claims of obtaining a special discount off list price for its new airbuses. PERC says that Air Lanka obtained a discount of around 25 per cent on their six airbuses and a most favoured customer status, where the airline will be compensated if Airbus Industries offers the same or better deal to any other customer. But an Asian Wall Street Journal report titled 'Boeing's woes persist and Airbus gains', (April 27) says, "So both companies have slashed prices - frequently 20 per cent off list - and grabbed all available business" If Air Lanka negotiated six airbuses at 20 per cent discount and entitlement to a further 5 per cent or so off if a better discount was given to another customer, then this does not seem to be a special at all. In fact as the Wall Street report says, the two heavyweights in the aviation industry, seem to be falling over themselves to offer discounts to all customers in a duopolistic frenzy for a large slice of the aviation cake. After Boeing swallowed Lockheed Corp. and McDonnell Douglas, its market share in commercial and military aviation shot up to 60 per cent, a figure they are obsessed with protecting at any cost, the Wall Street report says. The Asian Wall Street Journal' quotes Boeing's CEO, Mr. Condit: "the most fundamental issue is that we're moving from a period where our products were defined by their performance to a period where costs are more important." While this is definitely good news for all customers, Air Lanka included, is this so called 25 per cent discount anything special? PERC chief, Dr. P. B. Jayasundera confirmed that Air Lanka has obtained most favoured customer status where the airline is entitled to a rebate if Airbus Industries offers better terms to other customers. He however added, "Depending on the buying power anyone can get it (these terms)." So, is the US$550 re-fleeting exercise negotiated on such "favourable financial terms" as a PERC media release claims?

Declining industrial exports need responseThe latest trade statistics bear evidence of the impact of the South East Asian crisis. The export figures for the first two months of this year compare unfavourably with those of 1997. The export growth of only 4 per cent in the first two months compared to the same period last year is a poor performance. This is especially so as there has been a high growth in agricultural exports of nearly 17 per cent. The agricultural export growth has been almost entirely due to a rise in tea exports, while rubber exports dipped and rubber production dropped by nearly 6 per cent. Industrial exports grew by only 1.4 per cent. The impact of South East Asia's devaluations have been marked in some sectors. Garment exports withstood the devaluations owing to the high import content, quotas and a shift of some of our garment manufacturers to specific quality garments. Although some garment manufacturers fared badly owing to the competitive pricing of South East Asian countries, garment exports grew by 9 per cent in the first two months. As was expected, rubber export manufacturers suffered most. Rubber goods exports have been disrupted by both the devaluations and the lower world economic growth. Rubber exports, which had been growing in the last several years and absorbing a higher proportion of our rubber production, experienced a drastic decline. Rubber and leather exports declined by nearly 12 per cent in the first two months. This is indeed one of the most unfortunate reversals of an export which showed considerable promise and one in which it was thought Sri Lanka had a comparative advantage. The category of 'other exports' too have shown a marked decline of 38.7 per cent. This decline in 'other exports' is indicative of several high raw material based exports suffering from the price competition of South East Asian producers of similar products. The country needs a policy which would enable us to withstand such an external shock, which could be temporary, but have a long term impact, if appropriate countervailing measures are not taken. It may be opportune for the government to assist rubber manufacturers, perhaps even stockpiling rubber at current prices, with a view to their utilisation later. A scheme of assistance which would negate the specific impact that the devaluation has had on rubber products is needed, not only for the sake of rubber manufacturers but also the large number of small producers of rubber. The currency crisis in South East Asia should not be allowed to disrupt what is intrinsically and fundamentally an industry in which Sri Lanka has a comparative advantage. The large investment in rubber manufactures should not be allowed to go waste because of a temporary setback. The problems of the rubber manufacturers and the producers would have to be looked at differently. In the case of the manufacturers, there would be no escape from sourcing raw material at the lowest international prices. Even that would be inadequate if other production costs are higher in terms of foreign currencies. In the case of the rubber producers, they require to be assured of adequate returns to maintain their livelihoods. Fortunately many small producers are part-time. This may give them some resilience. Yet the income from the small holdings is critical for their basic living needs. Plantation companies which have diversified holdings are able to bear the shock much better. Their profits in tea would enable them to withstand this crisis. We hope the plantation companies would adopt a strategy which not only enable them to withstand the current crisis, but also one which would ensure the long-term productivity of their rubber lands. Overall, macro solutions may not be adequate to cope with the emerging impacts of the South East Asian crisis. There is an urgent need to adopt specific policies which ensure the long-term viability of critical industries. At the same time there must be adequate flexibility and change to cope with future trends in world economic developments. We hope someone is looking into these aspects of vital economic importance to the country.

Is capital account liberalisation a good idea? The pros and consIs capital liberalization a good idea? What lessons can be gleaned in this area from the financial crisis in Asia? Is amendment of the IMF's Articles granting it jurisdiction over capital movements necessary, or should the IMF continue in its present role supporting the process of capital account liberalization under its present Articles? These and other related issues were discussed at a seminar hosted by the IMF on March 9-10. The seminar was held at the behest of the IMF Executive Board to elicit views from a wide range of private and official opinions outside the IMF. Participants included high-level government officials, banking and investment officials from industrial and developing countries, academicians, and representatives from international organizations. IMF senior staff management, and Executive Board members also participated. The trend toward capital account convertibility is "irreversible," IMF Managing Director Michel Camdessus said in a luncheon address on March 9, and "all countries have an important stake in seeing that the process takes place in an orderly way," no matter where they stand on the opening of their own capital accounts. The benefits of open capital markets, Camdessus said, are well known: free capital movements help channel resources into their most productive uses and thereby increase economic growth and welfare nationally and internationally. Countries at all levels of development can share in these benefits. As David Peretz of the UK Treasury said, "This is not a subject on which industrial countries and developing countries should divide. There is a common interest in getting it right." For developing countries, as the traditional sources for financing have dried up, access to international capital markets to finance their current account deficits has become essential to their continued growth and development, according to Muhammad Yaqub, Governor of the State Bank of Pakistan. Without open capital accounts, these deficits may simply not be "financeable at desirable levels of investment and growth." Despite its acknowledged widespread benefits, however, free-flowing capital can exacerbate financial crises that threaten the stability of the international monetary system. As Lawrence Summers of the US Treasury noted, "Global financial markets let us go where we want more quickly and, most of the time, more safely than was possible before. But the crashes, when they occur, are that much more spectacular." Certainly, massive capital flows played a role in the financial crisis in Asia. Yet, the imposition of capital controls on foreign borrowing except in certain specific cases does not appear to be a workable solution and, in fact, would be a step backward, according to Summers. Charles Dallara of the Institute of International Finance agreed, citing the "significant risks" to capital controls. If the trend toward open capital movements is irreversible, and if the benefits to be realized from free access to capital markets are undeniable, how, then, can the costs and risks be minimized? Three themes emerged from the discussions: preconditions, orderly and steady progress toward full capital account liberalization, and the IMF's assumption of jurisdiction over capital movements. Preconditions Although no one was willing to say with any certainty how long a country should hold off opening its capital accounts, there was consensus, according to IMF First Deputy Managing Director Stanley Fischer, that "liberalization without a necessary set of preconditions in place may be extremely risky." The absence of such preconditions could promote a crisis or reveal weaknesses in the financial system that could have been overcome if the authorities had been allowed more time to strengthen the system before the capital markets were opened. An unresolved issue is how to determine when an economy is sufficiently prepared in terms of preconditions to risk opening the capital account. Some participants expressed the fear that too much talking about preconditions might discourage countries; they would then end up waiting forever for preconditions to be in place. Some participants suggested that change does not happen until it is forced. Much of the source of the financial crisis in Asia could be traced to lack of attention to structural issues, according to John Lipsky of Chase Manhattan Bank. Conventional wisdom has tended to place the blame on freely flowing capital often in the form of short-term debt that washed over the shores of unprotected countries with weak domestic institutions. In fact, the real culprit was the unwillingness of governments to expose their institutions to market discipline by raising interest rates to stem capital flight and refusing to unpeg their exchange rates. As a result, the crisis spread from country to country in the region. The importance of sound and consistent economic policy cannot be overstressed, according to John Heimann of Merrill Lynch. But helping to prevent or lessen the impact of future financial crises requires strong measures on the domestic regulatory side: prudential standards, disclosure requirements, and transparency. Important conditions for capital account liberalization mentioned by several participants included: o a sound macro-economic policy framework; in particular, monetary and fiscal policies that are consistent with the choice of exchange rate regime; o a strong domestic financial system, including improved supervision and prudential regulations covering capital adequacy, lending standards, asset valuation, effective loan recovery mechanisms, transparency, disclosure, and accountability standards, and provisions ensuring that insolvent institutions are dealt with promptly; * a strong and autonomous central bank; and timely, accurate and comprehensive data disclosure, including information on central bank reserves and forward operations. Orderly progression Capital movements certainly played a major part in the financial crisis sweeping through much of South-East Asia, according to Jack Boorman, Director of the IMF's Policy Development and Review Department. But it was not open capital accounts per se that led to problems. In fact, the economies in the region with the most open capital accounts Hong Kong SAR and Singapore have been the most successful in contending with the crisis. Rather, the difficulties in the hardest-hit countries Indonesia, Korea, and Thailand arose from the prevailing macro-economic environment and institutional setting and the way in which capital liberalization was brought about. The most relevant lesson from the Asian crisis, Boorman said, was that capital account liberalization must proceed in an orderly manner. Yung Chul Park of Korea University and the Korea Institute of Finance concurred, citing the Korean experience. The "gradual and piecemeal approach to liberalization" the authorities pursued so as not to disrupt the economy, he said, proved a failure; during 1994-97, Korea still experienced a surge in foreign inflows much of it short-term and speculative. For emerging market economies, the improper management of the opening of financial markets could, he said, "easily lead to a boom and bust cycle during the transition period." 'The capital account should be opened gradually, according to Carlos Massad, President of the Central Bank of Chile, to protect the economy from unregulated inflows particularly of short-term capital that, because they are quickly reversible, can seriously dislocate the economy. In Chile's case, the authorities have imposed controls on inflows with apparent success, bringing about a steady drop in short-term indebtedness. At the same time, as Yung Chul Park noted, a piecemeal, ad hoc approach can also be disruptive. With the gradual approach undertaken by Korea, for example, it was difficult to determine the sequencing for the deregulation of the different types of capital account transactions, which markets should be opened, and the speed with which the liberalization should move. Roque Fernandez, Minister of Economy, Argentina, also noted that in Argentina's case, prudential controls over the banking system, rather than controls on capital inflows, had proved effective in handling the risks of short-term capital inflows. Since capital flows are now a fact of life, the chief concern is how best to achieve an orderly process of liberalization. This process, David Peretz said, should be overseen by the IMF and the Articles should be amended to make this jurisdiction explicit. Although the IMF has encouraged countries with IMF supported reform programs to free up their capital accounts, legal jurisdiction would allow the IMF to apply the principles of capital liberalization to all member countries through its surveillance activities. The IMF is the ideal agency to undertake this function, he said, because it could deal with each country on a case-by-case basis, adapting the liberalization process to the country's individual capacity and complementary structural reforms. Jacques Polak, former Director of the IMF's Research Department, emphasized the advocacy role of the IMF. He argued that amending the Articles, although not necessary, would be useful. But, he said, giving the IMF formal jurisdiction over capital flows would be neither necessary nor helpful. In the past, he said, the IMF has moved into areas not specifically covered in its Charter, such as governance. Because the IMF has wholeheartedly embraced capital liberalization in its surveillance, financing, and technical assistance activities despite the lack of mandate and the provisions of Article VI condoning capital controls it is not necessary to give the IMF jurisdiction in order to liberalize capital movements. Amending the Articles to give the IMF such jurisdiction might take the IMF beyond its area of competence and might also bring it into conflict with other institutions, such as the World Trade Organization, he argued. On the other hand, David Peretz noted, one of the reasons for defining the IMF's jurisdiction would be to reduce conflict with other organizations. Addressing the legal ramifications of the IMF's jurisdiction over capital movements, Francois Gianviti, General Counsel of the IMF's Legal Department, said that the IMF could not effectively assume such jurisdiction under its present Charter. The other tools provided by the Articles (technical assistance, surveillance, and conditionality) could not achieve a comprehensive, uniform, and permanent liberalization of capital movements. Only an extension of the IMF's jurisdiction to capital movements through an amendment of the Articles would enable the IMF to achieve this objective. Manuel Guitian, Director of the IMF's Monetary and Exchange Affairs Department, said that the IMF should assume explicit jurisdiction over capital movements, to emphasize commitment to the orderly liberalization of capital accounts. Without commitment, he said, advocacy carries little conviction. A country's resolution to open its capital account and its agreement not to impose restrictions at a later date would not be credible without the commitment, transparency, and conviction imparted by its obligations as a member of the IMF to proceed toward an open capital account. The IMF needs to participate in the formulation of universally applicable principles and a code of conduct to guide the liberalization process, Guitian said, thus ensuring that the process of liberalization is orderly. This code of conduct must reflect current events; if it is too far behind reality, it will lose credibility. But the actual speed with which countries move toward full liberalization would depend on individual cases. During the process, they would have recourse to transitional arrangements analogous to those available for procession to current account convertibility. What is important, Guitian said, is that a country commit to general principles; individual commitments could then be determined by all member countries, as they are for current account convertibility. (IMF Survey)

A measure of underlying inflationIn its 1997 Annual Report, the Central Bank discusses

the need to decompose the permanent and transitory components of

price changes in the measured inflation indicator so as to derive

the "underlying inflation" or "core inflation"

as against the "headline inflation" as reflected in the

original price indices. The discussion is contained in Box 4

of the Report and it is reproduced here. Table 2

|

|||||||||||||||||||||||||

|

Headline and Underlying Inflation Rates |

||

|

Headline Inflation |

Underlying Inflation |

|

|

1996 Jan |

8.4 |

11.7 |

Source: Department of Census and Statistics Central Bank of Sri Lanka

In Sri Lanka inflation is generally measured by the Colombo Consumers' Price Index (CCPI) which is the official price index computed by the Department of Census and Statistics (DCS).

The Greater Colombo Price Index (GCPI) computed by the DCS is also used to measure inflation. The other major indicators of inflation are the GDP deflator and Wholesale Price Index computed by the Central Bank of Sri Lanka.

Maintaining prices at a low and stable level is the primary objective of monetary policy. Ideally, all prices should be fully determined in the market, and stability in such unregulated prices would be a reflection of overall macro-economic stability and the effectiveness of monetary policy in containing inflation.

There are permanent and transitory components of price changes. Therefore, for effective policy formulation, it is essential to decompose the two components in the measured inflation indicator. In this context, it is necessary to exclude the effects of temporary shocks from the price indices so as to derive the 'underlying inflation' or 'core inflation' as against the 'headline inflation' as reflected in the original price indices. In measuring underlying inflation, countries use various methods to eliminate supply side shocks.

In the United States, for example, sub components of the consumer price index such as food and energy prices are excluded. Food prices are excluded as they are volatile and erratic while energy prices are excluded on the grounds that they are determined by the Government and as such, are largely unrelated to demand pressures in the economy.

In the United Kingdom, mortgage interest costs are excluded from the headline rate in order to obtain the underlying rate.

In Sri Lanka prices of several consumer goods, i.e., wheat flour, bread, kerosene, electricity, transport fares, cigarettes and liquor are administratively determined by the Government. Among these items with 'administered' prices, wheat flour, bread, kerosene and tobacco have high weight (with a combined current weight of about 16 per cent) in the CCPI and thus, price changes in these items have considerable influence on inflation.

The prices of these items were revised on several occasions during the last two years (Table 1).

In arriving at an estimate of underlying inflation, these items should be excluded from the basket of the CCPI and the price change in the residual basket can be used as a measure for underlying inflation.

In early 1996, the effect of the sharp reduction in the administered prices of bread, wheat flour and kerosene in the latter part of 1994 continued to be felt in the inflation rate measured by the unadjusted CCPI and therefore, the unadjusted rate fell below the underlying rate. (Table 2).

Similarly, adjusted for upward price revisions effected since April 1996, the underlying inflation rate lies below the headline rate from July 1996 onwards.

However, the above is not an exact measure of core inflation. It still inherits the various weaknesses of the CCPI and further refinements need to be made to obtain a more appropriate indicator of core inflation in Sri Lanka.

Table 1

|

Administered Price Revisions, 1996-1997 |

||||

|

Item |

Unit |

From |

To |

Date |

| Wheat Flour Bread Bus fare Wheat Flour Bread Cigarettes Coconut Arrack Wheat Flour Bread Kerosene Oil Cigarettes Wheat Flour Bread Electricity |

1Kg. 450g (loaf) Approx 15% 1Kg. 450g (loaf) 25 cts-50 cts increase 175.00 1Kg 450 g (loaf) 1 ltr. 25cts. Increase 1Kg 450 g (loaf) |

11.95 |

12.45 |

April 1996 April1996 July 1996 July 1996 July 1996 July 1996 July 1996 Aug.1996 Aug.1996 Sep. 1996 June 1997 Aug. 1997 Aug. 1997 September 1997 |

Source: Central Bank of Sri Lanka

Regional Issues

More Business * V-bomb sets poser on SAPTA's future * Stress on plant efficiency pays dividends for Kabool * Golf decided Lanka it is * International Training Centre * Commercial Bank tops growth figures

![]()

Front Page| News/Comment| Editorial/Opinion| Plus | Sports | Mirror Magazine

Please send your comments and suggestions on this web site to