|

9th August 1998 |

Front Page| |

|

Venture capitalist - the equity partnerBy Harim W. PeirisA venture capitalist or venture capital fund is essentially an equity partner in a business. As an equity investor, the Venture Capital (VC) shares the risk of the business. Unlike a lender, an equity investor has little or no recourse to the assets of the business, which would be mortgaged to the lenders. As a risk taking partner the VC expects corresponding high returns, that would only realize should the business perform. As such the VC analyses an investment more thoroughly than a lender, to fully understand the business risk being assumed. Some people wrongly assume that the venture capitalist is an unsecured lender. An unsecured lender would demand a higher rate for the greater risk, but cap the returns to a predetermined rate. The VC is not a lender, it is not a bank. They are institutional business partners that provide risk capital. In the mature financial market of the USA, venture capital funds have focused on technology start up companies and received annual returns of 35%. However, in the Asian region and the UK venture capitalists have also ventured into manufacturing and services, especially at the expansion stage and for Management Buyouts (MBO)/ buying. Again, UK venture capitalists have received returns in excess of 30%, p.a. on financing MBOs. Funding and structuring Management Buyouts has been another success story for VC in developed financial markets. A Management Buyout (MBO) is a transaction through which management acquires a substantial stake in an often effect control of the business it has managed, usually through financial arrangements tailored to suit individuals of relatively modest means. A management buy in (MBI) is when a manager or team of management buys into a company also using financial structures geared to assist individuals of modest means. The purchase of an existing business eliminates the risks and costs inherent in a start up venture. MBOs and MBIs are very popular in more developed financial markets and competent managers are buying companies within the industry in which they have expertise at an increasing rate. However the Sri Lankan market on the surface does not provide the most hospitable environment for a buyout of a business. Many businesses are family owned or closely held and a business venture is perceived as a store of value and wealth in an increasingly inflationary environment. However a closer look at the economic landscape provides many opportunities for successful purchasers of existing businesses by competent managers. The Government of Sri Lanka's privatization programme provides many opportunities for the purchase of State owned ventures that need new management to turn them around and run them efficiently and profitably. Family businesses with succession problems or a lack of managerial skills after several generations provide opportunities for management buyouts, businessmen migrating and large companies selling off peripheral business units are other avenues through which businesses can be bought. Thus the MBO can produce significant gains to both the buyer and seller of the business. Venture capitalist participating in MBO and MBI eliminates the cash constraints that potential management buyouts face and arrange the equity structure of the target company in a manner that would enable the management team to begin with a small equity stake that would increase over time through bonus shares based on performance. Various other hybrid structures and balance sheet arrangements including investing through different classes of voting, non voting, ordinary and preference shares enable the VC to provide management control to the owner managers while retaining adequate protection for their investment. Funding business expansion through venture capital funding is a particularly attractive option for both the VC and the business owner. Many businesses start up small with the entrepreneurs own or family funds and reach a stage where a stable business could give much greater returns if operated on a larger scale, i.e., namely a business expansion. Often the lack of corresponding assets to seek loan/debt finance and limits on prudent gearing prevent a small business from growing through either debt/loan financing or internally generated funds. In such a situation a venture capitalist with an infusion of fresh equity into the business would move it from a small business to a medium scale company. For the VC an expansion stage funding eliminates the risk of a start up business and provides an existing track record with which to appraise the business. The entrepreneurs also benefit as the VC recognizes the value of an existing business and provide the zero cost equity capital while holding a minority ownership position in a business. The Venture Capitalist (VC) seeks companies that have competent managers, high growth potential or hidden value. A venture capital firm usually takes a minority equity position in an investee company for a medium term period of typically four to six years and then exit the investment either through a listing on the stock exchange, a sale to a third party or less preferably a sale to the owner managers. A venture capitalist provides a unique financial niche product, namely risk capital assuming equity style risk in the venture for equity returns from the business. Venture capital financing is often though equity and quasi equity type investment instruments and venture capitalists seek returns that are very much higher than debt lenders who base expected return on average interest rates. Venture capital is a nascent industry in Sri Lanka, a relatively unknown financial intermediary whose existence hasn't been much publicized due to its relatively small size when compared with the development financing institutions such as the NDB and DFCC and the commercial banks. However venture capital firms have been operating in Sri Lanka for over a decade, with three being listed on the Colombo Stock Exchange. Venture Capital funds in Sri Lanka have invested with individual entrepreneurs with sound existing businesses and also alongside large multinationals in well-known large companies. The writer is a Senior Investment Analyst at Ayojana Fund Management (Pvt) Ltd., which manages two venture capital funds, namely NDB Venture Investments and Ayojana Fund.

More crop per dropThe United Nations Food and Agriculture Organization (FAO) has announced a major international initiative to improve irrigation and drainage in developing countries. A budget of over US$ 6 million is being negotiated with the World Bank, the UN Development Programme (UNDP) and other donors for a three-year plan of action . "World population will jump from today 5.8 billion to 8.3 billion people by 2025. To meet this challenge we have to produce more food through the intensification of rain-fed and irrigated agriculture," said Programme Manager Arumugam Kandiah. "Irrigation more than doubles land productivity. Unfortunately, many irrigation systems are working poorly, due to bureaucratic interference, faulty management, lack of involvement of users and poor construction. In some cases up to 60 percent of the water diverted for irrigation never reaches the crop." "In addition, in many regions water scarcity is already a major problem and seriously limits agricultural production. Water is becoming increasingly limited and costly, and farmers are under pressure to grow 'more crop per drop'. To do this, they need to know more about appropriate, efficient and sustainable irrigation technology." Irrigation technology in developing countries has not changed much during the past decades and is seriously lagging behind the agricultural technology it serves, according to FAO. Annual global expenditure in irrigation research is no more than about US$ 300 million compared to about US$ 8 billion in agriculture as a whole. "Through the International Programme for Technology Research in Irrigation and Drainage (IPTRID) we want to support farmers in finding the most cost-effective, user-friendly and socially-acceptable irrigation and drainage technology. The programme will not finance irrigation projects, but will promote technology transfer and make applied research information on irrigation drainage available to farmers and decision-makers." "We will also assist in developing national irrigation research and development strategies. Partners will be the ministries of water and agriculture, non-governmental organizations, universities and the private sector," Kandiah added. "The management of the programme will be small and decentralized," Kandiah said. "The five-person Secretariat based in Rome will work through national committees and research institutions." The IPTRID was founded in 1991 and originally run by the World Bank. The programme assisted in financing of some 15 projects valued at about US$ 50 million. Information was provided through ten country networks with more than 5,000 participants. Dissemination of knowledge and capacity building will play a bigger role in future. The World Bank therefore decided to move IPTRID to FAO, a more specialized organization with a wealth of expertise in irrigation. The World Bank will remain a co-host of the programme along with UNDP, the International Commission on Irrigation and Drainage and the International Water Management Institute. Among the major national sponsors are the United Kingdom, France and the Netherlands. Spice office bearers Spices and allied Products Producers' and Traders' Association recently elected the following office bearers:. Chairman: Chris Dassenaike, Director Marketing, Free Lanka Management Co. (Pvt.) Ltd; Vice Chairman: S. De Silva, Director, Intercom Ltd. COMMITTEE Exporter Representatives: Informex Trading (Pvt.) Ltd., V. Abeyratne; Link Natural Products (Pvt.) Ltd., Dr. D. Nugawela; Meera Saibo & Co. (Pvt.) Ltd SH, M. Nazar; Meezan & Co. (Pvt.) Ltd., S. A. Cader; Saboor Chatoor & Co. Ltd., G. S. Chatoor; and Stassen Exports Ltd., P. Fernando. Producer Representatives: Elpitiya Plantations Ltd., R. Fernando; EOAS International, D. A. Perera; Gamewasama Estates Ltd., M. C. M. Zarook; Kegalle Plantations Ltd., R. Pillai; P. W. Rodrigo Estates Ltd., J. Rodrigo; and Uda Pusellawa Plantations Ltd., J. E. de Silva.

BOYA - a man who moves debt markets

.By Mel GunasekeraQ: When was the first Commercial Paper introduced and how did it come about? A: The first Commercial Paper (CP) was issued in 1993 when I was working for Mackinnon and Keells Financial Services. At that time, the Treasury Bill (TBill) rate was over 21 per cent and the corporate borrowing rate went up to 19-20 per cent. At that point, we had to find alternative ways of reducing corporate financial funds. My Director, Ajith Fernando and my Group Chairman, Ken Balendran told me to find a way to reduce their costs. As I came from the Bank of Ceylon (BoC), we studied the set up as to how a banker raises money, what are the problems the banks are facing and we tried to find an alternative to the traditional way of borrowing. Our company had pledged our securities, we were having overdrafts and short term loans. From the banks' point of view, they not only loan but also invest money. So we went to the banks and said why don't you invest with us. You are 100 per cent backed by security. The BoC also felt the need to develop the debt market. On a trial basis BoC agreed to structure a CP. They accepted our concept and said they would join hands to develop the market. We issued a paper, a pro note (promissory note) for three months to the BoC. They discounted the paper and sold it to the public. At this point I must mention the role the BoC played in the development of the debt market. It was a turning point in our banking industry in the disintermediation process. The first step was on 6th August 1993, when the BoC discounted the Rs. 25 mn John Keells paper less than the TBill rate. TBill rate was 21 per cent, they discounted the paper at 18.7 per cent. It was a bold step and I must mention that if not for BoC this wouldn't have been a reality. With this issue, we went to other corporates, while simultaneously structuring another Rs. 50 mn paper for Aitken Spence. McKinnon and Keells Financial Services structured both issues. Q: People say you are the 'father of the CP concept' is it true? A: Yes I introduced the concept, but to implement it we need all parties. The disintermediation process began from this first step. Q: Do you see a revolution in the banking industry since CP was introduced? A: Yes. Now the corporates are going for fixed and floating rate borrowings. The banks also lend on a floating rate, because they also have to match their liabilities. The CP concept was the first step towards developing the debt market. Since then, we have seen a lot of corporate debt, medium term debts coming out. Disintermediation is the answer to develop the market. I got the autonomy from my management to structure the product and they gave me the fullest co-operation. You can't do things without autonomy. I really enjoyed the autonomy I had at John Keells. I was at the right place to do it. From the banking sector I moved on to the corporate sector and I was able to see how the corporates worked. That's how I was able to come up with innovative products to raise funds for corporates. Q: Why did you choose CP as a way to raise funds? A: We began with CP as people are not used to long term debt instruments. So we decided to go short term with CP. To develop a market you must start small, short term, medium term and long term. Q: At what stage of development is our debt market at the moment? A: When you talk of debt, you must see where you are going to place it in the market place. Only four debts have been listed on the stock exchange so far. That means we are still in the initial stage. My answer for the 21st century is disintermediation, as the bankers too have their own problems. The banks are burdened with reserve requirement problems, assets and liabilities, mismatch and capital adequacy. At the corporate level they have to pay BTT, Defence Levy. The only way, which they can overcome this, is by disintermediation through securitisation. For this, more debt must come into the market. Q: How do you see the growth of the CP market? A: Over the last five years we have seen the growth of the CP market with over 40 corporates issuing their own CP. Now the people have the appetite. From the corporate point of view, most companies have their own treasury division. They are looking at various means to reduce their financial burden. Q: Do you see a change in the traditional way of borrowing and lending? A: The traditional way of borrowing and lending is changing. You have to add value to securitising. Other products must come in. With this, the old traditional borrowing and lending habits would fade away eventually. The blue chips would go directly into the market. Lots of debenture issues are coming out, and are to be listed on the stock exchange. Down the line, many people are talking about their long and medium term loans. On the other hand, the government is also trying to develop a long-term yield curve by issuing government bonds instead of TBills. It's a healthy sign. We have given the lead and we want others to follow. Q: Why is our debt market at such a primary level, what is needed to develop it? A: Traditionally our people still believe in the banking system. In the early 1980s, many finance companies collapsed. With this, people lost confidence and confined themselves to commercial banks for lending. We have to give alternative ways for people to decide. Various investment products for people to decide, because of the risk reward structure. Q: Do you think people are still unaware about the risk reward structure? A: Yes. People need to understand why they need to invest for the future. The credit risk, liquidity and return. In our country people have forgotten the return factor, they are instead getting a negative return for their investment. They are getting poorer and poorer. We have to first address this situation. For any investment decision we know low risk low return, high-risk higher return. In Sri Lanka, the banking sector is giving a negative return to their savers. The public has to be educated first, to see not only the credit risk but the return as well. They have to understand the risk reward structure first. In the meantime, new products must come in, then the appetite will be created. Q: So, what is the stumbling block to the growth of the debt market? A: The government is paying a higher return on TBills than the banks, this is the stumbling block in the debt market. This is the anomaly in the risk reward structure. I said low risk low return. But at the last auction, a TBill went up to 13 per cent. Whereas, the bank deposits are around 9% -11%. At a 2% - 3% per cent difference, how is the government going to pay a higher rate again? Its going to effect the budget deficit, this is today's risk, which is what you and I are paying. The government is borrowing to uplift the poor, whose money is going into the banking system in the form of savings. But the saver can help the government by purchasing a TBill. Then there will be more demand for the TBill, the prices will decline and there will be more stability in the interest rates. Then the debt market will develop. See the bond market. Two-year bonds are going at 13 per cent. What is a four-year rate? How can you structure a risk? We saw two debentures come in, Commercial Bank and Hatton National Bank at 14.2 per cent. At what rate are we going to discount it, if the two year bond is going at 13 per cent? We can gear the market, but we must first put the foundation right. We need to correct the anomaly in the risk reward structure. This is the key to the development of the debt market. My main thing is that awareness is very important, correct the anomalies and automatically the others will come right. Now we have gone up to 4-5 year debentures, and the bond market would be developed up to 10 years. From DFCC's point of view we are committed to develop the debt market, with value addition. Q: Have you seen a progress in correcting the anomaly in the risk reward structure? A: Yes. If you want to develop a market the awareness is important. You have to protect the saver. There are a lot of organisations to protect the borrower but very few to protect the saver. We can't develop the market on the ignorance of the saver. We have to give the right dues to the saver. The biggest problem in our country is that our savings ratio is 17.3 per cent of GDP compared to India's 26 per cent of GDP. We have to accelerate our savings. It's our national duty to give a better return to our savers. We should not use the ignorance of the saver to make money. There has to be a balance, the saver must be educated to understand the risk reward structure. Q: Has any progress being made so far? A: The Central Bank, specially the Public Debt department has realised this. They have appointed 18 primary dealers to deal with government securities. Out of the 18 dealers, 14 are commercial banks and the rest are financial institutions. Now the Central Bank is in the process of changing the system because they found that commercial banks are not interested in selling TBills. Under the new system, if you want to be a primary dealer, you must have a dedicated primary dealer operation, whose full time job is to broadbase the TBill market. The government is taking a positive step towards it. To develop a debt market you need awareness to sell it. We can't operate a debt market without hedgings. You must offer balance sheet and off balance sheet hedgings. In 1994 after introducing CP, lot of corporates came into the CP market to borrow short term linking the interest rate to TBills. In 1993 we saw a volatility in the TBills, then the corporates were looking at alternative hedging mechanisms to hedge against TBills. Q: What was the next product you were involved in introducing to the debt market? A: In 1994 Mackinnon and Keells Financial Services introduced the first forward rate agreement (FRA) to Singer Sri Lanka for a short term period. At that time, the leasing companies were trying to back their assets and liabilities, they were managing four year leasing programmes on a 3 months roll over basis. In 1995, when our interest rates went up to 107 per cent, they realised they must come to the fixed rate or floating rate. The banks were willing to give a floating rate but the borrowers wanted a fixed rate. We structured the first interest rate swap for LOLC. There are over Rs. 1 bn interest rate swaps outstanding at present. We then introduced interest rate caps, with LOLC. The BoC came forward for this as well. Interest rate collars were introduced by LOLC with Union Bank in 1996. Q: What are the other tailor-made products that can be issued to the market? A: The SEC is now trying to work out on a futures market. This is a healthy sign. When we talk about international market we talk about options, derivatives, forward rate agreements, futures. These are all products, which can be introduced here. What we want is awareness. First of all at the management level. If the Treasurer is to sell the product to the board, they must be in a position to understand what he has to say. Q: Isn't there a hesitation at the management level? A: Yes. When you talk about the derivatives, the collapse of Bearings Bank and Nick Leeson come to mind. I compare derivatives to a knife. A knife is useful for our day to day operations. You can also stab a person with a knife. Is it the fault of the knife or is it how you use it? Derivatives can be used for three things; as a hedging tool, as an arbitrage and as a trading tool. If we use this instrument as a hedging tool, you are only hedging your risk. You need control. Q: It can be argued that for the development of the debt market complete de-regularisation is necessary. But what are the dangers of opening up the capital account? Can we draw parallels to the East Asian crisis? A: We have seen the examples of East Asia. When our savings ratio is low, and you encourage foreigners to invest in the country, what will happen on the day they decide to pull the plug? What happened to East Asia would happen to us. The Central Bank is on the right path now, to put the infrastructure in place. George Soros once said, "You don't depend on the foreigners, you increase your domestic savings". We have to develop our domestic savings to prevent us from falling into similar situations. Q: Do you think the Development Banks are offering the best range of products to the development of the capital market?. A: Yes. You will see the policy of how DFCC is going to contribute to this positively. This is the key to develop our market. We have the expertise and we are now putting the infrastructure right. We did a test run with the Ceylon Glass Company debenture issue. You will see a lot of debt being introduced to the market very soon. Q: What role would the rating agency play in the development of the debt market? A: .To develop the market further, we need a rating agency. A rating agency will give third party information only. But the investor themselves should be able to take a correct decision to understand the risk reward structure. All of us must get together to develop the risk reward structure, in order to develop the debt market. By converting the savings into TBills and bonds we are helping the budget deficit to come down. Awareness is important and more products are needed. Q: Is everything in place for the debt market to take off in a big way? A: Yes. But greater awareness is needed at the corporate level. I want to protect the saver. We should not take undue advantage over the ignorance of the saver. It's our national duty to protect them. By giving a better deal to the saver, we create a healthy banking system and a healthy debt market. The banks are also coming out with debentures, this is a good sign. But, we have to educate the public to identify the risk and take the correct decision. By frequently talking about these issues we can develop a healthy debt market. We need to get products tailor - made to suit our needs. I don't want to take the credit for all these products. The credit should go to all the institutions and the people I worked with. It's a joint effort. I am also thankful to the BoC, who taught me the ABC of banking and finance. As a state bank, I have my gratitude to them. We had only the concept. Bank of Ceylon is a premier bank, they are the ones that taught the ABC to me. Ruhuna 2001 on AirRuhuna 2001 Multivision Pvt Ltd. (Multivision) has signed an agreement with Home Box Office (HBO) Asia for the distribution of its two premium movie channels on its soon-to-be-launched wireless cable system in Sri Lanka, a company release says. "HBO is the pre-eminent carrier of top quality motion picture entertainment in the world with over 33-million cable television subscribers,'' said Teb Boyle, President and CEO of Multivision. HBO Asia is the television arm of HBO Pacific Partners, a joint venture of Time Warner, Paramount Films of Southeast Asia, Universal Studios and Columbia/ Tristar.

Industrial Relations ForumQ1: "Can an employer withhold gratuity from a workman whose services have been terminated for reasons of fraud, misappropriation of funds, willful damage to property of the employer causing loss of goods or property of the employer". Please state the relevant section of the Gratuity Act. Yes, please refer to section 13 (page 8) of the Gratuity Act no: 12 of 1983. Q2: I am employed in a private firm as an executive for the past 5 years. My letter of appointment states that I have to give 3 months notice before I leave the company. But certain members who joined in the same capacity subsequently/previously had only one month notice in their appointment letter. Please tell me whether it is necessary me to give 3 months notice and what will be the consequences if I didn't give any notice or one month's notice.? You have already accepted the term to give 03 months notice before leave the company. If you leave giving only one month's notice, the employer can take legal action against you before courts. However , he cannot deduct the amount involved from your salary or other statutory payments without your consent. Q3:Is Saturday a holiday for Mercantile Establishments and Government Establishments Saturday is a half-holiday for shop/ office employees in mercantile establishments. In the case of government employees it depends on the orders made by the government. At present, it is a holiday for government employees. Q4: I am employed at a leading Gems and Jewellery Company and retired at the end of March this year after 12 year's service. I filled up the relevant forms to claim my EPF and ETF and handed it over to the Company. Subsequently I made several calls to claim my gratuity, EPF and ETF and the response has been negative. Their excuse is that they don't have the money to pay me. I have been reliably informed that EPF and ETF monies have not been credited to the Central Bank for the last three years. The chairman of the company has taken temporary residence abroad and there is no sign of him coming in the near future. What what is my plight? You are legally entitled to receive gratuity, EPF/ETF. Therefore you may make an official complaint to the commissioner of labour, who will take legal action against your employer to recover the gratuity, EPF/ETF due to you with surcharges. Q:5 I had been an employee of a leading Five Star Hotel in the city, from the period 1988-1995, during which period the hotel had been in the practice of retaining 10% of the service charge payable to the staff, against breakage and damages to the hotel property, without any intimation to the staff member. After intervention from the trade union, this retention was finally paid to the staff currently in employ somewhere early this year. I, being a past employee had requested hotel to release my outstanding dues, for which I have been told that the Hotel has not taken a decision in this regard. What course of actions should I take, as this is a substantial amount of money, which is due to me? Please make a written complaint to the commissioner of labour regarding this issue Q6: Are Executives in mercantile Establishments entitled to overtime payment for working after working hours, Saturdays, Sundays and Poya days? Executives are required to work full time for the establishment. That is why they are paid a higher salary plus other benefits. Executives in public sector as well as mercantile sector are not entitled for overtime. Q7: I wish to inform you that the Employees' Provident Fund Act No:15 of 1958 came into operation on June 1, 1958 and the regulations framed there under ensure retiring benefits to employed persons by means of a contributory provident fund. Contributions by both employer and employee must be on the total earnings, which has been defined in the Act and in the Regulations as: a) Basic salary or wages However, a foreign bank operating in Colombo, chose to operate an Approved domestic provident fund. Under the regulations of the EPF Act of Sri Lanka, approved domestic provident funds must satisfy the requirements that the amounts of contributions made by the Employer/Employee to the domestic fund should not be less the contributions they would have made to the EPF. From the very inception of the operation of the bank employee's provident fund and up to 1992, the rates of contribution to the Fund by the Employee/Employer were 5 percent and 10 percent on ONLY the basic salary of the employees. However, in 1992with the signing of the Collective Agreement by the Ceylon Bank Employees' Union and the SBI Management, the statutory requirements of the EPF rates of Employee/Employer, became 6 percent and 12 percent on the total earnings of employees. In view of the discrepancies in contributions to the fund, can I rightfully claim payment of deficiency from the Bank from 1961 (my date of Appointment) to 1992 since I retired from the Bank in 1995, and since I do not have funds to enter into litigation, what is the mode of recovery of the deficiency due to me? To answer your question please provide the following information |

|||

|

More Business * ARCASIA plans package for architects * ITI to begin course in business administration * Qatar Airways presents awards* Egypt unveils new shipping hub plan * Alliance adds more to transport service* Who are the FACTORY EMPLOYEES? * SLIM workshops on Management Development * Business Diary * Business Diary * MMBL to invest in financial services * Indian software giant moves to Colombo * SLCB pushes MICE tourism * Commercial Bank opens branch at Vavuniya * SIA shifts to new home * China Airlines - SIA in Alliance * Impressive growth for Pramuka Bank * Hayleys offers the 'Intelligent Film'

Front Page| News/Comment| Editorial/Opinion| Plus | Sports | Mirror Magazine |

||

|

Please send your comments and suggestions on this web site to |

||

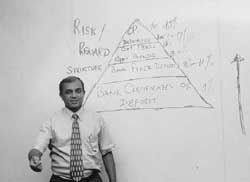

Mangala

Boyagoda, is a name synonymous with Sri Lanka's capital market, more specifically

its debt market which slowly but surely indicates signs of opening up.Hardly

anyone is more qualified to talk about its slow, even sluggish development

than a banker who was Bank of Ceylon's chief dealer for over a decade and

a trail blazer in bringing short/medium term money instruments into the

local debt market. Mangala Boyagoda's (simply "Boya" to many

in the industry) enthusiasm and energy are infectious and his vision and

commitment to developing the debt market formidable.With a deep-rooted

sense of social justice,Boyagoda says that raising debt capital for corporates

and banks should never be at the cost of the poor saver. His drive and

desire to educate the saver on an accurate "risk reward" basis

has taken him to many a forum - from schools, academia to high powered

financial workshops - where he displays the same passion to give the best

return to the saver and thereby increase the savings rate in the country.

Boyagoda was involved in structuring the first ever commercial paper, a

pro note when he was at Mackinnon and Keells Financial Services and speaks

of it almost like his favourite child. He has come a long way since, moving

from Union Bank to his current position as DFCC Bank's Director Treasury,

an ideal position for him, before he goes onto bigger and better things...

Mangala

Boyagoda, is a name synonymous with Sri Lanka's capital market, more specifically

its debt market which slowly but surely indicates signs of opening up.Hardly

anyone is more qualified to talk about its slow, even sluggish development

than a banker who was Bank of Ceylon's chief dealer for over a decade and

a trail blazer in bringing short/medium term money instruments into the

local debt market. Mangala Boyagoda's (simply "Boya" to many

in the industry) enthusiasm and energy are infectious and his vision and

commitment to developing the debt market formidable.With a deep-rooted

sense of social justice,Boyagoda says that raising debt capital for corporates

and banks should never be at the cost of the poor saver. His drive and

desire to educate the saver on an accurate "risk reward" basis

has taken him to many a forum - from schools, academia to high powered

financial workshops - where he displays the same passion to give the best

return to the saver and thereby increase the savings rate in the country.

Boyagoda was involved in structuring the first ever commercial paper, a

pro note when he was at Mackinnon and Keells Financial Services and speaks

of it almost like his favourite child. He has come a long way since, moving

from Union Bank to his current position as DFCC Bank's Director Treasury,

an ideal position for him, before he goes onto bigger and better things...