Economic growth is likely to fall to 6 per cent this year as external and internal shocks are serious setbacks to the country's economic growth.

The Central Bank has not revised its economic growth forecast for the year, but current conditions suggest that economic growth would slip from 7.2 per cent that it estimated earlier this year to even below 6 per cent, if global demand for exports continues to be unfavourable and the prevailing drought conditions persist. The falling international oil prices are the one favourable development that could mitigate the economic slide.

Global conditions

The international economic downturn is widespread. Even China's state capitalism has been unable to weather the global storm and the Chinese economy is expected to slow down this year. The Indian economy may experience a precipitous decline in its growth. India's economic progress that had been impressive in the last decade has been halted and its first quarter economic growth dipped to just 5.3 per cent. India's slower growth could affect the Sri Lankan economy in several ways. India is an important trading partner. About 5 per cent of our exports are to India.

Furthermore, foreign investors tend to view investment prospects regionally. India's troubles could intensify foreign investor concerns on Sri Lanka as a destination for FDI. Moreover our long term economic expectations are linked to the fortunes of India.

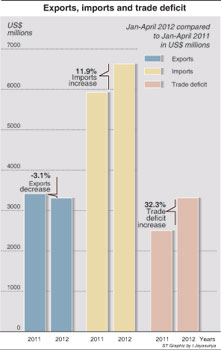

The most pertinent global developments for Sri Lanka in the short run is the instability of European economies that have slowed down and reduced their purchasing power of commodities exported by us. European countries and the US that accounted for 54 per cent of our exports last year is a sizeable one for industrial exports. The decrease in exports to Europe is being felt in the trade statistics this year. The American economy too has not recovered adequately, and this being an election year, is not expected to regain a growth momentum. With these two main markets affected, our industrial exports have faced a drop of 3.1 per cent in the first four months of the year.

What is particularly disconcerting is that there is a trend of decreasing industrial exports, especially of garments. In March industrial exports declined by 10.2 per cent and in April it declined by 8.7 per cent, compared to the respective months of last year. Tea exports to the Middle East and Russia too have been adversely affected and in the first four months, tea exports decreased by 11.8 per cent, contributing heavily to the decline in agricultural exports by 11.7 per cent compared to the previous year's first four months. Total exports declined by 3.1 per cent in the first four months of this year compared to the same period last year. Indications are that both industrial and agricultural exports would face adverse conditions and are not likely to recover.

Imports

Imports continue to make a serious dent in the trade balance. Although consumer imports declined by 3.3 per cent, intermediate and investment goods continued to increase. Imports were much higher than exports and resulted in a trade deficit of US$ 3.3 billion in the first four months. If this trend continues the trade deficit could be as much as US$ 10-11 billion. This would certainly strain the balance of payments as it is too large to be bridged by worker remittances, tourist earnings, other service earnings and capital inflows. The expectation of higher amounts of foreign direct investments is unlikely. Therefore once again there would be a drain on reserves or increased foreign borrowing to meet the trade deficit, as well as repay capital borrowed earlier and to service interest payments.

Economic stability

The stabilisation of the economy is becoming an uphill task with exports declining and imports continuing to rise. Consequently the trade deficit is continuing to widen even though some imports are showing signs of decelerating. The exchange rate has depreciated as much as 17.5 per cent since Nov. 21, when the government devalued the rupee by 3 per cent.

Global conditions are no doubt at the root of the problem. The economic policies pursued in the recent past too were not modified to take into account the realities of the global situation and the unrealistic path of development that was pursued, without consideration of resource availability and balance of payments implications of the consumption-investment pattern.

Internal shock

As if the external shocks are not enough, the country is in the throes of a severe drought. While the hopes are that the monsoon is a delayed one, the current expectations are that a severe drought is likely.

This is likely to reduce paddy as well as other crop outputs in the main paddy growing areas. It is estimated that the Yala 2012 crop will decline by about 30 to 40 per cent. There may be a need to importing rice this year. If international rice prices increase then it would result in a further strain on the balance of payments.

The impact of a drought on the capacity for hydro electricity generation is serious. Increased thermal generation would necessitate higher petroleum imports. The gains by the reduction of oil prices could be wiped out by increases in the amount of oil imports. Meanwhile in the first four months of this year import expenditure on oil increased by 34 per cent.

Silver linings

There are a few silver linings amidst these dark clouds. International oil prices are falling. Though, as usual, there is volatility in oil prices, they are hovering at a much lower level that in the early part of the year. Oil prices of around US$ 90 per barrel could be a significant boon. Complementing this is the US decision to exempt Sri Lanka from the ban on oil imports from Iran. This too could bring some relief with the possibility of importing Iran crude on concessional and differed payment terms.

Worker remittances that are an important source of funding the trade deficit are continuing to increase. In the first four months remittances increased by 16 per cent compared to that of the comparable period last. This is good news in a context when there was considerable uncertainty about remittances growing owing to the turmoil in the Middle East.

Policy imperatives

Only about one half of the probable trade deficit of US$ 11 billion is likely to be offset by remittances. Tourist earnings that are increasing may finance about 10 per cent of the trade deficit. Therefore the current account deficit would have to be financed largely by either running down the reserves or through borrowings that are contingent liabilities. In this context every effort must be made to reduce imports through appropriate pricing policies, reduction of government expenditure and conservation measures. Reducing the price of petroleum products would be an inadvisable measure.

|