|

12th July 1998 |

Front Page| |

Contents

|

||

|

Mind your businessBy Bsiness bugAd ban Recently we wrote of how advertising agencies would be hard hit by the ban on alcohol and tobacco promotion from next year. Now comes the news that government is reviewing the laws governing the use of children in advertising. If some have their way, the use of children under 14 years of age in public advertising could be banned, or alternatively, severely restricted. We all know most advertisements now use children, so it could be another telling blow for the ad industry . Debentures are the hottest things in town. The banks have completed highly successful issues and the glassmaker's issue is bound to be oversubscribed. One state bank is planning an issue but so are several other blue chips, we hear. The stock exchange meanwhile, is taking a long hard look at this phenomenon Industrial Parks There has been a lot of publicity about the industrial parks that are to be set up in the Siyane Korale. But things are not so rosy as those propaganda press communiqués would have you believe, they say. The reason? Investors are fighting shy of dumping their money in the park, not knowing what its fate would be if the parties in power change. So much so that generous tax incentives are being contemplated to lure investors .

Minority shareholders left in the lurch?By Mel GunasekeraMinority shareholders are accusing the Colombo Stock Exchange (CSE) of washing their hands off errant companies instead of taking action to correct and penalise offending companies and officials. The Colombo Stock Exchange announced last week that nine companies who have not submitted audited quarterly accounts for years will be de-listed on July 31. Minority shareholders say they bought shares in listed companies because of regulation and transparency, and the CSE cannot suddenly dump them and expect the shareholders to carry out the fight on their own. People buy equities in listed companies because they are regulated, and they do not expect the companies to be taken out of regulatory framework because CSE finds they are unable to effectively regulate them, they said. The nine companies are: Upali Investment Holdings Ltd. (audited accounts outstanding from March 31st 1997), Mercantile Credit Ltd. (audited and quarterly accounts outstanding from March 31st 1991), Ceylon Match Company Ltd. (audited and quarterly accounts outstanding from March 31st 1992), Champs Development Ltd. (audited and quarterly accounts outstanding from March 31st 1992), Electro Holiday Resorts Ltd. (audited and quarterly accounts outstanding from March 31st 1992), Magpek Exports Ltd. (in the process of winding up), Compak Morrisons (Lanka) Ltd. (assets taken over by NDB), Lanka Carbons Ltd. (under liquidation), and Carsons Marketing Ltd. (office, workshop and warehouse premises sealed by State Bank of India). Trading on all these companies is already suspended and de-listing them was the next step, Director General CSE, Hiran Mendis told 'The Sunday Times Business'. When a company is de-listed the usual procedure is for the majority shareholders to buy out the minority stakeholders. But in the event of the CSE de-listing the company, the minority shareholders are left out in the cold. "Minority shareholders will have to seek recourse under the companies act," Mr. Mendis said. It is part of our obligations to inform the shareholders of the situation, which is why we inserted a press notice," he said. Analysts say this might set a bad precedent because directors can simply de-list their companies by violating the CSE rules and buy out minority shareholders at their leisure or not buy them at all. Unless the CSE has a procedure where companies are forced to be de-listed, companies are compelled to buy out minority shareholders. Financial sources say the Securities and Exchange Commission (SEC) has the necessary legislation to bring errant companies to the notice of the Registrar of Companies, to force them to publish their accounts. This method has been successful in the past, with companies including Upali Investment Holdings fined and made to toe the line. New investors should be warned the moment a company stops publishing its accounts, one analyst said. He suggested the CSE should indicate this in their daily trading notices. If an investor continues to buy shares of errant companies, they do it at their own risk, he said. Recommendations were made before to identify errant companies and prevent unsuspecting minority shareholders from buying those shares. The CSE had written to the errant companies last year asking them to bring their accounts upto date. But only a few companies responded. However, Upali Investments is on a better wicket than the rest of the companies. Business Times reliably learns that Upali's request for time till August 10th 1998, to bring its accounts upto date has been granted. The fate of the other eight remains unchanged. Four - Magpek , Compak Morrisons, Lanka Carbons, and Carsons Marketing, are beyond revival. Once de-listed, the company has to submit a fresh application if it wishes to seek a listing again.

Rupee will slide to 67.4 by year end says Soc-GenA top Colombo securities firm says the Sri Lanka rupee will depreciate to 67.4 rupees per one US dollar by the end of the year, from a current 64 rupees per dollar. The forecast by SocGen-Crosby Securities, the securities research arm of SocGen bank, follows regional developments and the fallout from the nuclear tests in India and Pakistan. If the forecast is proved right that would be good news for exporters but not consumers as the import bill would then rise, increasing the cost of consumer essentials. Some stockmarket analysts are hopeful that the impending meeting between Indian Prime Minister Atal Bihari Vajpayee and Pakistan Prime Minister Nawaz Sharif in Colombo during the SAARC summit on July 29, may bring some relief to the region and also ensure the return of foreign investors. Political analysts however believe that the meeting may be a mere "we won't resort to nuclear tests if you won't do it" sort of parley and a major mending of the political fences is unlikely to take place. "But if it does happen - which would be short of incredible - then it would be a plus point for the region and would soothe the whole world," an analyst said. SocGen-Crosby Securities, said in its July report that the rupee depreciation accelerated as concerns about another currency crisis emerged in Asia. "Pressure built on the Sri Lanka rupee with a sharp decline in the Indian rupee and a falling Yen. The Indian rupee has declined by about 7.5 percent since the Indian nuclear tests and, in response, the Sri Lankan rupee depreciated by 1.3 percent during this period," it said. A combination of problems in Asia has hurt the Sri Lanka rupee. Last week, Central Bank officials told a news conference that the rupee has fallen by about six percent against the US dollar since January this year, compared to a depreciation of seven percent for the whole of 1997. When asked about the rupee's dollar value at the end of the year, Central Bank officials said they don't make any forecasts on the rupee. A depreciating rupee would of course cheer Sri Lankan exporters who have been clamouring for a better-valued currency to boost export earnings. Exporters and economists say the rupee is grossly over-valued in keeping with international trends. But in fairness to the Central Bank, its judicious mix of exchange rate policy and the management of fiscal policy measures was one of the reasons why Sri Lanka was able to withstand the regional financial crisis that hit East Asia and threatened to engulf the rest of Asia. That crisis however is not over and Sri Lanka is feeling the pinch in terms of the competitiveness of its exports.

Defence spending overruns estimatesBy Feizal SamathAs Sri Lanka's north-east military conflict intensifies, government spending on the security forces is increasing and has overrun this year's budget estimates, says a senior government minister. Deputy Finance Minister Professor G. L. Peiris told a meeting on Wednesday that spending on the military has gone over the estimated defence budget target of Rs. 44 billion for 1998. Defence spending in 1997 was Rs. 47 billion , Professor Peiris told a meeting at the Sri Lanka Foundation Institute organised by the United Nations Population Fund (UNFPA) to mark World Population Day. He did not give further details of military spending. Professor Peiris, in a wide ranging speech relating to population policies and strategies, dealt with law, health and education reforms, the economy, agriculture, poverty alleviation and suicides. He said that Sri Lanka was one of the countries in Asia that has achieved substantial progress in population policies and annual population growth rates were now at 1.2 percent. The minister, who also handles justice and constitutional affairs, said that there was a vigorous debate over what our priorities should be in population strategies. "Population policy is not merely about numbers. It has a lot to do with the quality of life of the people." Prof. Peiris spoke on current educational and health sector reforms being implemented by the government and on poverty alleviation programs which alone costs the government nine billion rupees a year. He said that agriculture was the backbone of the economy but sadly a proper marketing apparatus has not been developed to help the farmer.Prof. Peiris referred to the creation of dedicated economic centres, the first of which has been set up in Dambulla, which will provide proper refrigeration facilities for stocking of produce, among other facilities. Proper storage facilities at the farms have been one of the biggest problems for Sri Lankan farmers and often vegetables are allowed to rot or are sold dirt cheap to traders in the absence of refrigerated facilities. The Food and Agriculture Organisation (FAO) is also working on providing proper storage facilities to farmers to enable them to stock excess produce and sell it during off season periods, which would thus permit an equitable distribution throughout the year and ensure reasonable prices, to both the producer and the consumer. Prof. Peiris said there were plans to set up these centres in several regions to ensure that the difference between the farmgate price and the price paid by consumers is not as wide as it is today because of high profits made by the middle man. "The middle man has a role to play in the agriculture sector but the profitability should be reasonable, not at today's levels. For instance, vegetables from Hambantota now cost eight times more than the farm price when it reaches the markets in Colombo," he said. Prof. Peiris said that the government and the World Bank were working on an ambitious programme of public sector reforms and pension reforms.

Wireless loop hurts telecom revenueSri Lanka Telecom (SLT) has cautioned that the continued loss of international revenue may hamper their rural expansion progress. SLT also says that the 35 per cent discount offered to wireless loop operators (WLL's) on international calls is hurting their revenue generated from international calls. "We want a level playing field with the WLL for tariffs on overseas calls," Christi Alwis Director Emergency Team SLT, said. At present, revenue generated from international calls is used to cross subsidise local call charges in Sri Lanka. Less calls originate from Sri Lanka to overseas countries has created an imbalance in the international tariffs. Since the imbalance is in Sri Lanka's favour, SLT is under pressure from world bodies like the International Telecommunications Union, the Federal Communications Commission (USA) to correct the tariff imbalance by reducing traffis on overseas calls. SLT also utilises the extra revenue to susbsidise its local operations and fund its expansion programmes. In 1997, SLT provided 80,000 connections. SLT hopes to connect a further 300,000 subscribers to its network by the end of this year, Mr. de Alwis said. However, the other telecommunication operators are not competing with SLT on an equal footing, a Telecommunications Regulatory Commission (TRC) spokesperson said. Unlike SLT, operators like WLL's have to fund their expansion programmes. They do not have additional revenue like SLT to subsidise their tariffs and expansion programmes, he said. The bulk discount of 35 per cent on outgoing overseas calls was included in the franchise agreement signed between WLL and Sri Lankan government. The agreement also states that WLL tariffs will not be regulated. "Though SLT's tariffs are regulated, we can't do the same with WLL's, as they will not be able to compete with SLT," TRC official said. The TRC is unable to assess the extent SLT is cross subsidising its local calls. Being an integrated service provider, and a government institution prior to privatisation, there was no need for SLT to maintain separate accounts like in developed telecommunication industries. Accounting separation is a necessity in a competitive environment. It is important to know the cost involved, hence the TRC has requested SLT to tow the line, but this would take time, TRC official said. Industry sources say SLT should welcome competition because traffic generated from other networks is generating additional revenue for investment to SLT at no cost. For instance, payphone operators do a yeoman service by servicing the public, but they are not given bulk discounts, industry sources said. It is necessary that they give discounts to bulk users like in other countries to develop the telecommunications industry.

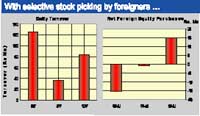

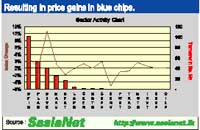

Political games boost market?

Some analysts believe that strong rumours filtering into the markets about a possible reconciliation between President Chandrika Bandaranaike Kumaratunga and her estranged brother Anura Bandaranaike, may have boosted sentiment at the market. While its fundamentals are strong, the Colombo market is sentiment-driven

and relies on an occasional burst of good political news to placate investors.

Analysts said that traders appeared to be swayed by the "feel good"

factor following reports - which were later denied by the president and

her brother - of an impeding meeting and indications that Anura Bandaranaike

will return to "There is a general feeling that Bandaranaike, in the PA, would be able to convince his sister to call off this unwinnable war and talk peace and also take on Deputy Defence Minister Anuruddha Ratwatte whose mounting challenge to the post of prime minister - once Mrs Bandaranaike calls it a day - is causing some worries in Bandaranaike circles," one analyst observed. By week's end though, the rumoured meeting was quickly denied by the government. A fairly widespread view in the stockmarkets is that government troops have got bogged down in a prolonged war and a growing belief that only a peace option will boost sentiment and help in a rally at the Colombo stock exchange. But an analyst at another top brokerage firm dismissed the political news theory saying that the reasons for the slight rise in the market was purely due to "cheap stocks" being available. "The regional crisis is the key factor that is pushing down our market and as long as it stays that way, the market is unlikely to pick up. What happened last week was that there were some bargains and some investors,

including foreigners, cashed in on this," he said. This analyst said

that the political climate, excluding the war The other possible "feel good" factor is the forthcoming provincial council elections which traders say would be an ideal opportunity to gauge public opinion of the government - after four years - in the wake of the war and disturbing reports of corruption and mismanagement. But analysts say that according to current indications, the polls may not be able and such a situation would be negative for the stockmarket. "If the polls are not held, I can only see the Colombo stockmarket going one way - down," one trader noted.

Strengthening the stock marketThe Colombo Stock Market has once again taken a nosedive. The underlying reasons for this dip in share prices was not the performance of the companies. In fact on the basis of corporate results both profits and growth led to an expectation of increased prices. It was at this very time that prices began to decline. The reasons for the sudden fall in share prices were no doubt due to global perceptions about the future of the region and foreign investors pulling out their funds. Fluctuations in the stock market are to be expected. This is not the first time that share prices have fallen. It has happened before and certainly this will not be the last time. Sri Lanka's market is particularly prone to such fluctuations owing to its high dependence on foreign investors who are notorious for shifting their capital from one market to another. Besides this, they operate on the basis of rules and guidelines which require them to shift funds no sooner there is a particular perception of the region. Their investments are often not related to the country performance but to the expected performance in the region. Today emerging markets are no longer considered good investments. Not so long ago, they were the places to invest in. The crisis in South East Asia sent shock waves to our part of the world as well. Additionally the economic sanctions on India and Pakistan subsequent to the nuclear detonations resulted in the South Asian region being perceived as a region to move away from. We require to recognise the realities of global investments and strengthen our own market in a manner that would give it a greater resilience. We should strengthen the domestic component of investments in order to make the Colombo Stock Market less prone to foreign investors' whims and fancies. This requires a number of steps to be taken to reduce the excessively speculative nature of the Colombo Share Market. One factor that would greatly enhance the stability of the market would be for large institutional investors to put more funds in the market, have a greater confidence based on the fundamentals of companies rather than be swayed by market sentiments, and to manage their funds in a professional manner. The professional management of share portfolios could assist in stabilising the market. Today it is far too much dominated by investors who use it as a casino. When the market goes up they buy for speculative reasons and when it dips down they sell. The result is an excessive swing in either direction and a market feeding on its own fluctuations. One serious flaw of the Colombo Share Market is that institutional investors themselves tend to opt out when there is a decline in prices. Some institutional investors are of the view that they have burnt their fingers and should not invest more funds. This is precisely the wrong logic. The price levels of most blue chip companies on the Colombo Share Market offer excellent value and investment opportunities. It's a time when institutional investors could put their funds in good stocks and expect to derive returns in the long term. Their increased investments would themselves propel the market upwards. Institutional investors must not look at the depressed Colombo Stock Market as a disaster. They must view it as an opportunity for investment. If these sentiments are shared by the large investors, their enhanced investments in the market would once again result in the Colombo Share Market turning bullish. Institutional investors could not only strengthen the market but also enable a larger inflow of funds for investment and the development of the capital market.

IMF shifts the blame"Those who thought the Asian crisis has abated have had a rude shock. Forecasters are again chasing Asian economies downhill". This is stated in an article by Robert Wade, professor of political economy in Brown University, published in a recent issue of the London 'Financial Times.' Having observed that Asia is in the grip of a debt deflation akin to the Great Depression of the 1930s, the writer poses the question: "How did it happen?" He says that the International Monetary Fund blames the national governments, the national governments blame outsiders and the populations blame some combination of the two. He calls this "the great game of shifting the blame," and asks "what does the evidence show?" Wade expresses the opinion that the nature of the IMF intervention has made things worse. In the first place, he says, the Fund insisted on far-reaching structural reforms in return for its bail-out money in areas unrelated to the immediate escape from crisis. This, he says, compounded the sense of panic by sending a signal that the economies were basically unsound, their good performance over the past decades notwithstanding. In the second place, the Fund imposed very high interest rates on the ground, as it supposed, that a sharp shock rise in rates would stabilise currency markets, damping pressures for competitive devaluations and making it easier for the governments in question to repay foreign creditors. But, in the event financial inflows did not resume and investors took the view that high interest rates were a signal of great dangers ahead, making them even more anxious to get out and stay out. The Fund failed to understand, says the writer, the implications of imposing high interest charges on Asian companies which were far more deeply indebted than their western or Latin American counterparts. High interest charges pushed them quickly from illiquidity to insolvency forcing them to cut back purchases, sell inventories, delay debt repayment and dismiss workers. Then, says Wade, banks accumulate a rising proportion of bad loans, their solvency comes into question, they call in loans and refuse to make new ones. Wade also contends that the IMF's insistence that banks adhere strictly to Basle capital adequacy standards only compounds the collapse of credit. The writer asserts that "the combination of high interest rates and Basle standards are the immediate cause of the wave of insolvency, unemployment and contraction that continues to ricochet around the region and beyond." He ascribes the reason for capital not returning, despite high real interest rates, to the uncertainty and instability which prevail and the risk of further devaluations. The writer wonders why the IMF has taken this contractionary approach when it is well aware of the US experience. After the 1987 stock market crash in which assets taken as collateral for bank loans fell sharply in value, the US authorities acted to keep markets highly liquid. Contractwise, says Wade, in Asia the Fund has acted to contract liquidity. He asks whether this is because the Fund is more interested in safeguarding the interests of foreign bank creditors than in avoiding collapse in Asia. Governments of the region, says Wade, must change their attitude of passive acceptance of the IMF prescriptions because the IMF approach is not working. They should, he says, set aside central bank orthodoxy that dominates current discussion, according to which very low inflation, restrained demand and high real interest rates are the top priorities. They need to take a tougher stance in the rescheduling negotiations with the creditor banks and lower interest rates to near zero. Also they should reintroduce some form of cross-border capital controls. Additionally, they should channel credit into export industries, generate an export boom and let the ensuing profits reinforce inflationary expectations, reflating domestic demand. On the question of capital controls Wade says that the West should "stop pushing developing countries towards a regime of capital account convertibility that includes free inflow and outflow of short term finance."

The European Central BankThe European System of Central Banks (ESCB) will consist of the independent European Central Bank (ECB) and the central banks of the EU member states. The European Central Bank will be managed by an Executive Board, which will comprise the President and Vice-President plus four other members. (see list below) The ECB will be responsible for the European monetary policy with the aim to maintain price stability and low inflation, below 2%, in Euro-area. The most important decision making body of the European System of Central Banks will be the Governing Council of the ECB, which will comprise the members of the ECB's Executive Board and the central bank governors of those EU member states participating in the EMU. In particular the Governing Council will decide on all matters relating to the monetary policy, which will be implemented only in those EU member states which have adopted the euro. The Governing Council had its first meeting on June 9, 1998. The Executive Board of the ECB will implement the single monetary policy in accordance with the guidelines set and decisions taken by the Governing Council. To this end the ECB will issue the necessary instructions to the national central banks. Board members 1. Wim Duisenberg (The Netherlands) President, a term of office of eight years. 2. Christian Noyer (France) Vice President, a term of office of four years. 3. Otmar Issing (Germany) Member of the Executive Board, a term of office of eight years. 4. Tommaso Padoa Schioppa (Italy) Member of the Executive Board, a term of office of seven years. 5. Eugenio Domingo Solans (Spain) Member of the Executive Board, a term of office of six years. 6. Sikka Hamalainen (Finland) Member of the Executive Board, a term of office of five years. (Courtesy European Union News)

Effects of the Asian currency crisisThe plunge in the Thai baht that began in early July 1997 quickly spread to the Philippines, Malaysia nd Indonesia. In late Octber, the regional crisis caused prices on the Hong Kong Stock Exchange to plummet, triggering a worldwide drop in stock prices. Japan's econcomy, tied closely to others in Asia through exports and investment, could also be affected, in turn exacerbating the current slowdown and instability of the financial system. The crisis in ASEAN (Association of Southeast Asian Nations) currencies that began with the Thai baht has been dicussed and analyzed in periodicals and reports by private research organizations. To more fully understand the economics, JETRO and the Institute of Developing Economies (IDE) carried out a joint research survey. The report began with a theoretical framework for understanding the currency crisis. It then took a comprehensive look at the economic prospects of the countries involved and the regional overall, including a detailed analysis of the currency crisis and government responses, as well as the economic and political background. The report looked not only at the ASEAN Four - Thailand, Indonesia, Malaysia and the Philippines - at the centre of the crisis, but also at the Republic of Korea, Taiwan, China and international financial centres Singapore and Hong Kong, a total of nine Asian economies. The report noted that fixed exchange rates, where a currency is linked, typically to the U.S. dollar, offer tremendous benefits, but have drawbacks. Excessive inflows of foreign capital, including short-term funds, swell the money supply when sterilization operations are insufficient. This leads to excessive purchasing power, an economic bubble and the malfunctioning of the financial system. At the same time, the country's export competitiveness falls as its currency becomes in effect overvalued due to rising inflation. Slower exports, worsening current account deficits and rising foreign debt throw economic growth into doubt. When investors decide matters have reached a critical point, they begin selling the local currency. The result is a currency crisis. Healthy Prospects Because of the currency crisis, a slowdown in growth in all ASEAN countries is inevitable for 1997 and 1998. However, while sharp drops are expected in Thailand for both years, the declines in Malaysia, Indonesia and the Philippines are expected to be relatively mild. Both the International Monetary Fund (IMF) and the World Bank believe that the currency crisis will not dramatically affect East Asia's long-term prospects. Growth can probably be restored through the reform and stabilization of financial systems combined with adjustments that help restore and promote exports. But if ASEAN countries are to compete with their rivals outside the region and ensure long-term growth, they must upgrade the structure of their industries, particularly their export industries. According to the report, this means converting to a pattern of growth led by improvements in productivity brought about by introducing new technology and developing a more skilled labour force. Japan Hit Hard The currency crisis has had a major impact on Japanese affiliates in the region. The cost of imported raw materials is expected to rise, while local demand for finished products will fall and competition will intensify among the ASEAN members. Some automakers shut down their operations in Thailand in 1997. At the same time, many firms failed to hedge their foreign- denominated borrowing, leading to enormous exchange-rate losses, which together with rising interest rates is worsening the economic situation. When many of the Japanese affiliates were asked about their medium- and long-term plans, they said that they would shelve new investment or expansion plans. But almost none was changing their overall ASEAN strategies. An important precondition of these strategies was the continued liberalization of trade within ASEAN. Japan is supplying financial aid, primarily through the IMF, to deal with the present currency crisis. In addition, it is expected to absorb East Asian exports, the report argued. Currently, East Asia is far more reliant on imports from Japan than on those from the U.S., although the opposite situation exists for exports. As a result, most East Asian countries maintain current account deficits with Japan. To support the continued growth of Asian economies, Japan is expected to help upgrade ASEAN exports at the same time that it improves its own domestic industries and imports more finished products from these countries. The views expressed in the report are those of the individual authors and do not necessarily reflect those of JETRO or the IDE. Courtesy Focus Japan

Switch back to Asia soonLatin American equities have significantly outperformed Asian equities since 1990, and especially over the last year but the next 6-12 months could well be a good time to switch back to Asia, according to Economics for Investment, the economics and finance publication of American Express Bank. The recessions in Asia have further to go, and the crisis has highlighted serious structural problems which will take a long time to put right. But most countries are implementing good policies now and economies should bottom by mid-1999. By 2000-2002, the region has a good chance of returning to strong 5-6% pa growth and this should lead to significant equity market gains. The countries likely to recover in the first wave are Thailand, Korea, Taiwan and the Philippines. The outlook for Latin American equities is not bad, but is unlikely over the long term to match the gains probable in Asia. Latin growth will slow in 1998-99 on the back of the Asia crisis and overheating worries. Growth will probably pick up later on the continued implementation of structural reforms but will be below likely Asian levels. Courtesy Economics for Investment.

Yeltsin says Russia will not devalue roubleMOSCOW: President Boris Yeltsin said on Thursday Russia would not devalue the rouble, despite a crisis draining its reserves, and markets drew comfort from progress towards an international rescue loan. "We have the capability...We have a plan of action (to avoid a devaluation)," Yeltsin told reporters before meeting his justice minister in the Kremlin. The 67-year-old president looked relaxed despite the tensions of recent weeks of fighting to save his economic reforms and prevent a deepening of political instability. But the central bank said foreign currency and gold reserves had fallen to $15.1 billion by July 3. The fall from $16.0 billion on June 26 indicated Russia was digging into funds needed to help meet debt payments in the next few months. Yeltsin gave no details of how the government would avoid a devaluation which economists say could spark inflation and widespread labour and social unrest. Coalminers are already blockading the Trans-Siberian railway to try to force the government to pay months of back wages, and isolated protests by disgruntled workers elsewhere have increasingly featured calls for Yeltsin's resignation. He and the cabinet have pinned their hopes of surviving the crisis without major social, political or economic upheaval on an emergency government plan and, above all, assistance from the International Monetary Fund (IMF). Anatoly Chubais, the Kremlin's top debt negotiator, told reporters that senior IMF official John Odling-Smee would arrive in Moscow on Friday for loan talks. "We should take decisions on the main questions," Chubais told reporters after the latest talks with IMF and World Bank officials on a $10-billion to $15-billion credit package. In Washington Odling-Smee told Reuters the IMF could manage to make a new loan to Russia, but after large Asian rescue packages last year it would face a difficult situation in terms of its resources afterwards. Chubais said he expected a final decision early next week on support from the World Bank, which a source close to the negotiations said was considering bringing forward a structural adjustment loan for Russia totalling $500-600 million. The comments by Chubais helped Russian shares, which have fallen heavily this year amid a crisis of confidence partly caused by economic problems in Asia and Russia's own woes. The Reuters real-time dollar-denominated RTS index was up 1.81 percent to 91.00. "The initial reaction to Chubais was very positive," a trader at a Moscow brokerage said. The rouble has been under fierce pressure for two months and rumours of a devaluation have regularly swept the market. The relative strength of the rouble and a reduction in inflation are two of the main achievements in the reforms Yeltsin has presided over. Their collapse would throw a pall over reforms in general and could have far-reaching political consequences. The central bank said on Thursday it had been tightening money policy to soak up roubles as Russian bankers warned a devaluation would lead to a disaster in the banking sector. Political pressure on Yeltsin is mounting steadily. (Reuters)

More Business * No remedy yet for ailing industries * Banking according to Islamic law * Life-Time awards for bankers * HNB debenture issue snapped up * Hemas' staff members celebrate 50 years * Hemas' staff members celebrate 50 years * shippings

Front Page| News/Comment| Editorial/Opinion| Plus | Sports | Mirror Magazine |

|

|

Please send your comments and suggestions on this web site to |

|

The

recent pick-up in Colombo's stockmarkets, after the initial crash from

June 29-July 3, has been attributed to several reasons which includes political

news.

The

recent pick-up in Colombo's stockmarkets, after the initial crash from

June 29-July 3, has been attributed to several reasons which includes political

news. the

People's Alliance fold.

the

People's Alliance fold. scenario,

was much stable in Sri Lanka than in India or Pakistan. "In that sense,

political developments at home are unlikely to be as effective as the regional

mood."

scenario,

was much stable in Sri Lanka than in India or Pakistan. "In that sense,

political developments at home are unlikely to be as effective as the regional

mood."