24th October 1999

Front Page|

News/Comment|

Editorial/Opinion| Plus|

Business|

Sports| Sports Plus|

Mirror Magazine

![]()

- Economy run by stargazers say brokers

- Vote on Account replaces budget

- Dread Bread

- CB may tinker with rupee trading band

- Mind your business

- Shy companies stunt DFCC's loan growth

- Budget delay may affect Paris Aid

- Economy needs a boost in the next century

- International finance architecture outmoded

- HNB chief on bank's new moves

- Wheels of the nation

- Japan gives Rs. 2.37m to grassroots bodies

- Commercial Bank offers high interest rates

- Deutsche Bank names regional head

- Pakistan puts pressure

- Elections announced; market hangs in balance

- Counterfeit phones on the rise

- YA TV notches four years

- CleaNet's aims to introduce cleaner production measures

Economy run by stargazers say brokers

Market analysts expressed dismay that political stargazers were driving the economy and expressed fear that the stock market and the economy may reach stagnant levels, with the postponement of the National budget to first quarter 2000.

It is rumoured that presidential soothesayers have advised her that her stars will shine brightly, indicating an election win this December.

Call money rates shot up from 14% to 15% last week, while banks reported that customers were hoarding dollars.

"The market will slide, interest rates will shoot up and futuristic things like local investment put off till the second half of next year," Director Research MMBL Phillips Securities, Nouzab Fareed said.

Economists also fear that the vote on account will be less transparent in the run up to a presidential poll.

"Postponing the budget is a big worry," says Chanaka Wickremasuriya, Head of Research NDBS Stockbrokers.

"We would like to have seen how the economy fared this year and how they propose to manage it next year. Future investments are depended on this," he said.

Though the government took a fairly tight stance in controlling its expenditure, the same could not be said about revenue collection.

"There are slippages in the collection side," says Dushyanth Wijesinghe Head of Research Asia Capital. The government was targetting Rs. 58 bn revenue from GST this year, but we hear they have so far got only Rs. 40 bn. "They (the government) is far below target as the GST collection is almost the same as last year," he said.

The pre-election announcement for reduced prices on sugar and flour may not make a dent in government finances. Wijesinghe says, world prices on flour and wheat have dropped down 50% and 40% respectively, due to low commodity prices.

The government made a profit on it so far. The reduction will only give away part of their profit, he said.

Analysts expected foreign direct investment to pick up in the second half of next year. Though FDI was US$ 85 bn for the first half of this year, analysts expect the P&O investment to offset any negative sentiments that may take place in the latter part of this year.

The elections have also come smack into the midst of the tourist season. The hotel and travel trade were expecting a healthy season, and with the millennium party coming out the industry was expecting a boom.

"If the campaign gets violent, it can have a negative effect on tourism," Wijesinghe said adding that the bulk of the tourists coming here belong to the budget category.

The hotel and travel sectors were expecting some relief by way of GST exemption from the budget.

But hotel sector analysts say though the hotel sector can pass on the tax, the travel sector may face difficulties. "We will have to absorb the cost but it will eat into our profitability next year," a hotelier said.

However, analysts felt the timing of the annoucement was somewhat of a relief.

"We all knew elections were around the corner, it was a case of when it was going to happen," says Rajiv Casie Chitty Head of Research CT Smith stockbrokers.

"Its better to get over the period of uncertainty," he said. But it will be a dull period of economic activity till the elections are over, he said.

"There could be a short term weakness in the market on somewhat inexplicable retail selling due to the news," says Amal Sandaratne, Market Strategist Jardine Fleming.

He said an early election is positive as it reduced the period of uncertainty and would reduce any political overhang on the market much sooner.

"The time period in which there could be potential voter give away's which would have a negative impact on the budget deficit, is also lessened."

However, there was common consensus on how much power the winner could get with a majority and how dependent the government would be on coalition partners.(MG)

Vote on Account replaces budget

With the announcement of the presidential polls and all political parties launching massive countrywide campaigns, the PA administration will present a brief Vote on Account November on the 11 and 12 to allocate finances until annual allocations are made through a budget proper, most likely in March next year.

The PA government has done away with the traditional five-day presentation in favour of a short one and a half day procedure at a time when the election campaign is expected to be in full swing.

The Vote on Account, does not permit capital expenditure, only recurrent expenditure. However there is no ceiling on allocations.

The Account while not dealing with the macro economic policy of the government or with the budgetary planning in general including development and other activities would be only a formal exercise where the finances for a specific period would be voted by the House.

While the prudence of this action is being hotly debated, a defeat of the Vote on Account would prevent the Parliament from authorising any spending from December 31 which marks the end of this financial year. However, a defeat would not prevent the opportunity of presenting more Accounts though there cannot be any presentations after the 31 of December before which all allocations have to be carried in the legislature.(DH)

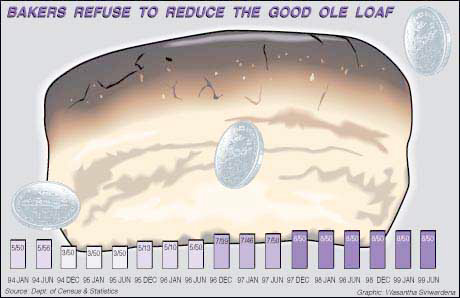

Dread Bread

Gone are the days when paang and paripu were the poor mans' bread and

butter. Today the good ole' loaf seems to have become a rather up market

commodity. The PA government's election promises to subsidise bread have

failed miserably and now the government is eating their words while  the

country is eating bread promised at Rs. 3.50 at Rs. 8.50.

the

country is eating bread promised at Rs. 3.50 at Rs. 8.50.

Last week the government reduced flour prices again in what was seen largely as a pre election gimmick especially in the context of the postponement of the annual budget, which was scheduled for November. (The government will have a Vote on Account pending the announcement of presidential elections announced for December). The reduction of Rs. 1.00 in a kilo of flour was shrugged off by consumers and bakers who said ti would not make a substantial difference in the price of a loaf of bread. Bakers are refusing to bring down bread prices claiming it was trivial sum and not practical to effect.

Bakers told the Business Desk that if at all the price was reduced, it would be reduced by 25 cents. Only one fourth the reduction in flour prices are reflected in bread prices because bakers claim that conforming to standards, only three loafs of bread could be made with one kilo of flour. Not all bakers were willing to even consider a reduction in bread prices and some dismissed it as an election stunt and felt that prices would soon escalate.

The modern day consumers (including the lower income groups) said they were not concerned if or not bakers reduced the price of bread, especially by a meagre sum of 25 cents, because historically the price of bread had anyway returned to the previous price or in times higher.

Also worth a mention is the fact that small denomination coins like 25 cents are really out of circulation now. How many of you on your many trips to the "handiya kade" have been charged an extra 25 cents by the mudalali, simply because he cannot give you back the exact balance? (SF)

CB may tinker with rupee trading band

By Mel Gunasekera

Central Bank is contemplating widening the rupee trading band, which in turn could lead to the rupee slide further, bankers said last week.

At present Central Bank daily sets the rates for US dollar/rupee within a two percent trading band for local commercial banks. Bankers say Central Bank may expand the band to three percent, to enable the rupee to slide between 30 to 40 cents.

A senior Central Bank official said the decision is yet to be taken, but Central Bank governor A S Jayawardene discussed the issue during last Friday's bankers meeting.

The band was last widened by one percent in 1995, which saw the rupee slide by about 30 cents. This is not the first time we brought this subject up for discussion, the official said. Even in 1997 it came up for discussion as our economy was stable and relaxed, but the onset of the East Asian crisis brought in a degree of uncertainty, the official said.

Another senior economist said the 'feeler' was put out because the balance of payment is recording a deficit this year after recording a surplus for the past two years. The government coffers were flushed at the beginning of the year because of DFCC Bank raised US$ 65 mn in the international money market through a floating rate note (FRN) but things have changed since.

There have been no major privatisation proceeds (privatisation target was Rs. 8 bn this year, but no exact figures are available as to how far the state is off target), only one small plantation company was listed and that too had no foreign proceeds and the expected monies from Sri Lanka Telecom has not come in as the IPO is fixed for next year. In 1997, major privatisation proceeds came from NDB and SLT, while in 1998 it was from the sale of Air Lanka.

The current account too is not flourishing due to poor stock market sentiments and fewer foreign direct investment, the economist said. One forex dealer said the rupee has been trading at the top end of the two percent band during the recent months indicating a demand for the US dollar.

The rupee is pegged to a basket of 25 currencies belonging to major trading partners. The rupee has been sliding at an annual 10 percent average against the US dollar, but has so far declined by about five to six per cent this year.

Mind your business

Poll secrets

The announcement from the lady that polls will be held forthwith caught everyone unawares including the Treasury Boys.

There they were, burning the midnight oil and preparing the speech for the good professor to read out on the floor of the House on the first and then they are suddenly told there will be no budget this year!

And some summoned enough courage to ask their boss whether even he was unaware of the impending announcement. Pat came the reply: "Of course, I knew but I was told not to tell you!"

Rotten deal

Cheap things are no good, they say and this is very true of cellular phones.

There has been a flood of offers of phones at dirt-cheap prices from many dealers in the recent past and customers are now finding that the promised performance has not materialized, leading to numerous complaints.

The complaints of course fall on the deaf ears of dealers and the established cellular networks say this state of affairs has not helped their reputations as well.

Their advice is to tell customers to ask for the bottomline- a comprehensive warranty. Then you are assured of some kind of compensation...

Shy companies stunt DFCC's loan growth

"Shy to list" companies are putting a strain on the lending growth of a leading development bank. DFCC Bank who raised US$ 65 mn internationally through a FRN (Rs. 4.4 bn) last year to finance medium to long term projects is experiencing a slower loan disbursement growth as companies are fighting shy of a listing.

In a bid to develop the country's debt market, the bank's lending policy stipulates companies to issue debentures within 18 months of receiving funds, which in turn should be listed on the Colombo Stock Exchange.

"So far we have disbursed around Rs. 1 bn but progress is a bit slow as companies are reluctant to go for a listing due to disclosure requirements under our laws," DFCC Bank Executive Vice President (Lending), L G Perera told The Sunday Times Business.

Perera says that most companies approaching them are family owned or closely held companies.

He said companies shopping around to borrow, are looking for a rate of about two percent lower than present lending rates. Listing is costly and therefore a deterrent.

DFCC was one of groups that lobbied the Stock Exchange to bring in a fresh set of rules for companies to list debt independent of equity.

The new debt rules were put out last month, but market participants say they are still too stringent to lure the big fish - family companies and big close knit corporates. Perera admitted progress was slow but said the bank was not unduly worried about the slow take off.

DFCC Bank raised US$ 65 mn in late 1998, through a ten-year FRN with a coupon of LIBOR plus two percent. The ADB guaranteed the principle amount, the government guaranteed the interest portion as well as effectively taking up the currency depreciation.

Under ADB regulations, DFCC Bank will create a sinking fund this December to pay back the loan. The lack of discount houses and secondary market liquidity is limiting the depth of the short-term debt market. DFCC Bank hopes to address this issue by setting up a bond house in conjunction with the International Finance Corporation and the National Savings Bank. The Bank is scouting for a technical partner at present. (MG)

Budget delay may affect Paris Aid

By Dilrukshi Handunnetti

Financial circles are expressing concern and doubt on the prudence of the government's decision to opt for a Vote on Account in place of a annual budget which generally reflects a country's financial status specially in view of the forthcoming Paris Aid Consortium sessions scheduled for December 14 and 15, authoritative sources confirmed.

Accordingly, the government which opted for the brief Vote on Account which would allocate specific amounts of money for a specified period would not reflect well on any third world nation dependent upon foreign aid for its development activities, the source said.

The Vote on Account which will be taken up on November 11 and 12 while not specifying the state's financial requirements and spelling out the PA's macro economic policy would merely seek to make contingent allocations until regular

allocations are made through the normal budgetary procedure.

What is termed as an 'imprudent financial decision' comes in the wake of the Paris Consortium expressing concern over several key issues marring the economic fortunes and interfering with its development activities.

According to highly placed sources, a warning has been issued to the Sri Lankan government that the forthcoming Consortium sessions would not be a pledging conference but a deliberative one only with the government's failure to tackle several key issues. The specified areas are macro economic policy planning, human rights, corruption issues, good governance and the settlement of the North East issue which has got prolonged and politicized in the process.

Accordingly, warning signals have been issued that unless good progress and keen undertakings are not visible to the donor community, the Consortium sessions would not be fruitful for the government which is struggling to keep the economy afloat while being burdened by a protracted war.

In this context, the non presentation of the regular budget is regarded as an unfavourable decision which would not auger well for the country in the eyes of donor nations keen to learn about the government's economic plans for the dawning millennium and specifically for the forthcoming financial year.

Economy needs a boost in the next century

The Central Bank has predicted or projected an economic growth of 4 per cent for this year. This appears optimistic in the light of only a 3 per cent growth in the first half of the year. The first quarter registered an economic growth of only 2.7 per cent and the second quarter only a 3.3 per cent growth in GDP.

While there are indications of some improvement, it is difficult to expect the growth in the second half to be as much as 5 per cent which is required to attain the hoped for growth of 4 per cent for the year.

Let's hope that the true figures turn out to be good. Let us not quibble with the figures. Instead let us consider what even a 4 per cent growth implies.

It means that in the second half of this decade Sri Lanka's economy grew at a lower rate than in the first. And that in the decade of the nineties we would have achieved an economic growth rate of only 5 per cent per year. When the decade began the expectation was an economic growth of 7 per cent per year.

This was deemed necessary to achieve NIC status or to put the economy on a growth path which would double income within the decade and reduce unemployment and poverty.

This was not to be.

Instead we are now talking in terms of the next year and the next decade, when we would be achieving a higher rate of growth. Achieving rapid economic growth appears to be like chasing a mirage....more a dream than a reality. What is even more disappointing is that the growth momentum has declined. In 1994 the economy grew at 5.6 per cent, in 1995 at 5.5 per cent and then at an alarming rate of only 3. 8 per cent. The economy recovered in 1997 to record a 6.4 percent growth but has kept declining since then to 4.7 percent in 1998, 3 per cent in the first half of the year and a projected rise to 5 per cent in the second half to yield a growth of 3 per cent for the year as a whole. We are only too aware of the reasons or excuses that are given for the slow growth.

Economists like to call them external and internal shocks. The tragedy is that no amount of shocks from whatever quarter appears to get our governments and our people alert and prepared to do the hard work to achieve higher economic growth. It is quite true that the Asian crisis, the Russian crisis and even the South Asian Nuclear explosion had serious impacts on our economy, but the most serious downfall during the decade was when we had a drought and a power crisis in 1996 accompanied by the bomb blasts of that year.

While there are no doubts about the various crises affecting our economy, a very trade dependent one, the real issue is what have we done for ourselves to ensure that we attain higher rates of growth. As soon as this government came to power there was a new expectation as the government decided to continue the open market policies. The continuity of policies gave a new impetus to economic development. Business confidence was unshaken owing to the policies laid out in the first Budget of the new government. As the government nears the end of its term that confidence seems eroded by a lack of proactive policies and an exceedingly slow administration. The government's preoccupation's are with the cracks in its own ranks, chasing a solution to the ethnic crisis which seems no closer than before, a rhetoric of bipartisan approaches which appears to separate the parties even more, and the pre occupations with a series of elections and next year's presidential and general elections.

No wonder the business community wants to wait and see till these issues are settled. The past decade is hardly the background preparation for the new millennium. Yet since hope stirs eternal in the human breast, let us hope that we are about to enter a new century and a new decade of lesser external and internal shocks and a government capable of leading the nation to higher levels of economic growth and prosperity.

International finance architecture outmoded

Dr. Bimal Jalan, Governor of the Reserve Bank of India recently delivered a lecture at the Centre for Business Studies of the Central Bank of Sri Lanka celebrating its 49th anniversary. He spoke on "International Financial Architecture: Developing Countries' Perspectives". A report of the lecture:

Dr. Jalan said it was an opportune moment to reflect on the subject as considerable international discussion had already taken place.

What he will touch on, he said, was more by way of reflection and some loud thinking "in order to advance our collective views on matters of interest to developing countries rather than final conclusions".

In the first place, it may be useful to understand why there is so much interest now in the new architecture; on what levels the debate has been conducted so far and how effectively developing countries have participated in this debate.

He would then deal with some of the major elements of the debate he said and finally highlight the institutional arrangements that have emerged or are in the process of emerging so that effective co-operation among developed and developing countries in monetary and financial issues could be facilitated.

Why the debate now

The global crisis that occurred after July 1997 generated enormous international concern over financial stability in the world, how to prevent such crises in the future and how to manage them if they do occur in the future.

This concern translated itself into a debate on these matters which included a review of the appropriateness of the existing financial arrangements and the need for redesigning such arrangements. Various facets of relevant reforms considered came to be known as the International Financial Architecture or IFA.

What were the reasons for considering a new IFA in the context of the current crisis. They were:

The recent crisis was sudden and unanticipated.

The speed with which the crisis spread took the financial community by surprise; new technology made capital flows easy and fast.

The failure of market mechanisms as were generally understood, necessitated a review of the relative roles of the state and the market in financial systems.

When the failure of markets resulted in systemic threats, the burden of market failure shifted to governments and the public sector.

There were questions regarding the timing, content and adequacy of the rescue packages extended by the IMF and other international financial institutions.

As the contagion spread across the world it became clear that developments in developing countries were important for the stability in the entire financial world.

Features of the debate

The experience with the Asian crisis led to the perspective that the existing international financial architecture was inadequate to meet the new realities. It started with an expression of dissatisfaction with the role of credit rating agencies and to some extent with the role of the IMF.

There was a shift in emphasis in favour of considering micro-economic aspects in addition to macro-policies, such as fiscal and monetary management. There was also a shift from abstractions to institutional aspects such as corporate governance, regulatory structure and transparency.

Finally, it was recognised that the divide between developed countries and developing countries was not as meaningful as it was thought to be.

Levels of the debate

The debate on IFA occurred at different levels and in different fora particularly the IMF and World Bank and also the UN. Other institutions engaged in the debate include the institute of International Finance, the international organisation of Securities Commissions and the International Association of Insurance Supervisors. Policy discussions were also conducted under the auspices of the G7 of the developed countries and G24 of the developing countries where Sri Lanka is currently in the chair.

The debate within these different fora and at different levels contributed to structured and formal discussions in the Development Committee and Interim Committee. These discussions were aided by informal and expanded high level official meetings of developed and developing countries; among these were G22 sponsored by USA, and G33 sponsored by G7. Another group was formed called the Financial Stability Forum.

Main issues in the debate

On the policy issues covered by the debate on IFA, Dr. Jalan focuses on eight issues which, he says, are of particular importance to developing countries. They are:

Exchange rate

Policy on reserves

Role of the external private sector

Management of capital flows

Strengthening of the financial system

Transparency codes and standards

Reform of international institutions

New arrangements for international liquidity.

The exchange rate

One view as regards an appropriate exchange rate regime is that a fixed exchange rate can promote domestic macro-economic and financial stability by providing a firm nominal anchor. But there are risks associated with a pegged exchange rate regime. Most of the currency crisis in the past two years have occurred in countries with pegged exchange rates.

A widely expressed view is that peg regimes should be eschewed in favour of either something much broader or the voluntary adoption of "managed floating".

It is also accepted that the degree of flexibility has to be "managed" in order to avoid undue volatility and panic. But yet there is no consensus on the modalities and the rules which should govern such "managed flexibility".

The role of the Central Bank to keep exchange rate movements "realistic" and relatively orderly has also been discussed. It is felt that stability in the conduct of monetary policy helps exchange rate stability. An increasing number of central banks, particularly in industrial countries, are directing monetary policy to the sole objective of price stability.

Increasingly near-term inflation targets are being announced. Transparency in objectives, intermediate targets and operating instruments are expected to play a role in anchoring expectations. But it is accepted, although not unanimously, that if there are unanticipated or unacceptable movements in exchange rates, central banks must be prepared to move interest rates to stabilise expectations.But it is accepted, although not unanimously, that if there are unanticipated or unacceptable movements in exchange rates, central banks must be prepared to move interest rates to stabilise expectations.

Direct intervention in exchange markets by the central bank may also become necessary. While developed countries are in a position to intervene in the exchange market on behalf of each other, such options are not available to most developing countries.

International reserves

The discussion on the optimum level of reserves has always been inconclusive. Traditionally, the adequacy of a country's reserves has been mainly linked to import requirements. But countries which held large levels of foreign currency reserves in relation to imports did not necessarily escape that crisis. These large reserves were expended swiftly as the countries tried to defend their currencies. Some part of these reserves could not be accessed when it was most required by these countries as they were invested in illiquid assets. Further, there was no transparency with regard to the precise figure of unencumbered reserves.

In the aftermath of the Asian crisis, the emphasis has now shifted from measuring the adequacy of foreign exchange reserves only in relation to imports to measuring the usable or unencumbered reserves in relation to short-term liabilities, in particular short-term debt.

It is suggested that emerging market economies should manage their external assets and liabilities (and the so-called "liquidity at risk") so that they will always be able to live without new foreign borrowing for up to one year.

The link between short-term debt and reserves has come up in the IFA deliberations. There is a cost to building up reserves through large debt flows; at the same time a high level reserve satisfies the need for liquidity, offers insulation against unforeseen shocks and acts as a source of comfort to foreign investors. All investments made out of reserves should be of top credit quality and excellent liquidity, the essence of reserve management being safety and liquidity. Hence the return on reserves and the cost of borrowing are not strictly comparable.

Role of the external private sector

The key issue concerning the role of the external private sector lenders and banks in forestalling a debt crisis, is whether by involving the private sector, the overall costs associated with foreign exchange crisis can be reduced. The idea is to institute mechanisms in place before the occurrence of any crisis so that the resolution of the crisis is more orderly

Ideas being considered include contingent credit lines, embedded call options, debt-service insurance, bond covenants, bankruptcy procedures, debt standstill and creditor debtor councils.

The mechanism envisaged would bind private sector participants to either provide additional funds or reduce debt service burdens in times of crisis without creating moral hazards or disruption to normal market conditions.

From the official sector, the IMF has decided to establish a contingent credit line (CCL) as a precautionary mechanism to ward off financial crisis. This is expected to supplement and not substitute the contingent credit lines from the private sector as in the case of Argentina.

Management of capital flows

After the Asian crisis, there has been an extensive debate on the issue of capital account liberalisation and controls. The issue is related to the desirability, form and content of capital controls, risk containment strategies in external debt management and the desirable sequencing of capital account liberalisation.

Overall there appears to be a consensus now in favour of developing countries restraining the inflow of short-term capital. But there is a growing debate in the means by which short-term flows can be controlled. There has also been a suggestion to impose an increased capital requirement on interbank transactions to bring about greater discipline on the cross-border interbank market.

It is self evident that there is no short-term borrowing without short-term lending. Unfortunately, in practice, the current policy is biased in favour of short-term bank loans rather than medium-term or long-term loans to developing countries.

Short-term loans to a country are likely to enjoy a higher credit rating than longer term loans, irrespective of the overall record of a developing country meeting its debt service obligations.

Three positions significant to developing countries seem to have emerged from the discussions on cross-border capital movements.

A case has been made for capital controls either as an emergency measure or as a temporary measure in a crisis.

Emerging markets should not liberalise capital accounts in a hurry, without prior action for strengthening their financial systems.

Capital account liberalisation should be supported by a consistent macro-economic framework, stable exchange rate policies and a strong institutional framework in the financial markets.

Furthermore, controls when necessary should be temporary and should be imposed on inflows rather than outflows and, as far as possible they should be focused on short-term volatile flows. A related issue is the possible amendment of the IMF's articles to extend its jurisdiction over the Capital Account.

Although from the view point of developing countries external capital has benefits and acts as a complement to domestic savings, short-term reversible flows can also have negative effects on the economy, particularly during periods of political or economic uncertainty. While large inflows pose policy dilemmas for macro-management, large sudden outflows can impose extensive damage to the financial sector and also result in a disproportionate output loss.

Each country should decide its own path of capital account liberalisation with regard to the timing and sequencing. It does not seem necessary to embark on a time consuming procedure for the amendment of IMF's Articles in order to promote capital account liberalisation.

A constructive consultative process between the IMF and member countries on these issues should be adequate to achieve the objectives in view.

Strengthening financial systems

Increased recognition has been given to three pre-requisites for the efficient functioning of the financial sector. They are: (1) a well designed infrastructure, (2) effective market discipline and (3) a strong and regulatory and supervisory framework. A well designed infrastructure has many elements. (a) a proper legal and judicial framework, (b) fostering good corporate governance, (c) comprehensive accounting standards and a system of independent audits and (d) an efficient payments and settlement system. Effective market discipline also requires a good credit culture and well developed and functioning equity and debt markets with a wide variety of instruments for risk diversification.

The Basle Committee is revising its existing capital adequacy guidelines. International consensus has already been reached on what constitutes sound practice in many areas of banking supervision and securities regulation.

Transparency code and standards

During the on-going debate on IFA, an influential view was that the information made available to the markets by the official sector or by corporate or by financial intermediaries prior to the crisis, did not reflect realities in the emerging economies. The practices of disseminating information as well as its reliability, timeliness and quality varied sharply from country to country. Hence, considerable attention has been devoted in the recent debate towards developing uniform transparency codes and standards.

It is important to recognise that while transparency is of paramount importance, as it enables and improves the understanding of the stance of policy by market participants, the quality and content of transparency have to be appropriate and in tune with country circumstances.

Given the divergence in institutional development and the nature of relations between various arms of national governments, it seems unlikely that a uniform code could be universally valid at this stage. It stands to reason that the accent should be on voluntary adoption and gradualism rather than a ''big bang".

International financial institutions

The discussions on the future shape of International Financial Institutions (IFIs) have revolved round three pillars:

(a) strengthening the existing financial institutions;

(b) creating new institutions; and,

(c) establishing new grouping.

IFIs must adapt to the changing environment if they have to remain effective, Principles that should guide efforts to enhance effectiveness include enhancing accountability, an inclusive process that facilitates a broad range of countries and other institutions and a more participative and open decision making process. The role of rating agencies has also been discussed. Ratings given by these agencies seemed to have influenced the decisions of investors in Asia and questions have arisen on the public accountability of these rating agencies.

Should they be used as they are or should they themselves be regulated? This is of importance in the context of the proposed New Capital Adequacy Framework of the BIS which envisages the possibility of assigning risk weights according to ratings. A proposal has also been put forward to create a new international institution called World Financial Authority (WFA) or a Board of Overseers of major International Institutions and Markets with powers for oversight and regulation globally. Various models have been envisaged for the proposed WFA.

It is well recognised that setting up such an institution would be a complex process. As an intermediate step, a suggestion has been made in the Development Committee recently for setting up a new and Permanent Standing Committee for Global Financial Regulation.

This intermediate proposal seeks to bring together not only the World Bank and the IMF, but also the Basle Committee and other regulatory groupings on a regular basis.

In response to these proposals, the major industrialised countries have now set up the Financial Stability Forum with representatives from the finance ministries, central banks and regulatory authorities of G-7 countries, as well as from the IMF, World Bank, Basle Committee, IOSCO, International Association of Insurance Supervisors, BIS, OECD, Committee on Global Financial System and Committee on Payment and Settlement System.It has been proposed that the Forum should be broadened by including participants from other industrial countries and emerging economies in order to make it more effective.

New arrangements

Finally, new arrangements are being discussed on the provision of international official liquidity to countries or financial markets, including the question of IMF being given the authority and the means to act as the lender of the last resort. The initiatives under consideration in this area can be summarised as follows:

It is generally agreed that the IMF should continue to play an important role in providing international liquidity. The major issues regarding adequacy of funds relate to increase in quotas, SDR allocation, sale of gold to augment the resource base, and increased borrowing from members. Proposals for enhancing the accountability and legitimacy of the World Bank have also received some attention.

In this context, there is suggestion that the Interim Committee could be transformed into a Council of Ministers. Reforming the Development Committee along similar lines has also been suggested.

As regards the proposal to establish an international lender of last resort, one line of argument is that there is no such need. A better approach to crisis management, it has been argued, would be to reform the debtor-creditor relationships, including introduction of provisions for orderly dept workouts and arrangements for temporary standstills.

In order to enforce emergency standstill and orderly debt workouts, a suggestion has been made to set up an international bankruptcy court but this has not been found feasible. As an alternative UNCTAD has suggested establishing an independent panel to determine whether the country concerned is justified in imposing exchange restrictions with the effect of debt standstills.

Thus, there is no shortage of new ideas on new institutions and new arrangements. However, a fair guess, at this point of time, particularly with improved prospects of countries in East Asia, is that the present institutional structure will remain more or less intact with some changes in operating procedures and management structures.

Conclusion

An important consideration that the international community must pay attention to is the hard reality that these new arrangements cannot operate successfully without equal partnership between developed and developing countries, or between capital surplus and capital deficit countries. The recent move to involve developing countries more closely in the discussion on the New Financial Architecture is, therefore, welcome.

But these efforts have not yet gone far enough. The institutional arrangements for decision making on the new financial architecture still remain too heavily weighted in favour of industrial countries.

The current focus is on measures to make the existing Bretton Woods institutions more effective and responsive. In order to achieve this objective, it is now essential to provide greater representation to developing countries on the Boards of these institutions, and to provide them with a larger voting power.

It is one of the ironies of the last forty years that although developing countries, as a group, have grown much faster than the developed countries over this period and their relative economic strength in terms of output and trade has increased substantially, their actual voting power in Bretton Woods institutions has tended to decline! This needs to be corrected in the next round of Quota exercises in the IMF and capital increase in the World Bank.

The Bretton Woods institutions have served the international community well. Therefore, the current consensus that there is no urgent need to create new international institutions is perhaps right. It is no longer possible for developing countries to delay the introduction of strong prudential and supervisory norms and structural reforms in order to make the financial system more competitive, more transparent and more accountable.

Finally for developing countries it is of utmost importance that we accord the highest priority to strengthening our banking and financial systems and bringing them up to the best international standards.

The role of financial intermediaries in mobilising and allocating domestic savings as well as external capital has now become crucial. This is an area where central banks like, yours and ours, have a special responsibility. In the SAARC forum, under the leadership of Sri Lanka, we have initiated measures to bring about better co-operation among our central banks and Ministries of Finance.

"We, in the Reserve bank of India, look forward to working closely with the Central Bank of Sri Lanka in moving speedily towards our common economic objectives," said Dr. Jalan.

![]()

Front Page| News/Comment| Editorial/Opinion| Plus| Business| Sports| Sports Plus| Mirror Magazine

Please send your comments and suggestions on this web site to

![]()

![]()