Inflation enemy number one: Dangerous and damaging

The large and growing budget deficit is to a good extent caused by the accumulated deficits of the past that has built a massive public debt over many decades now. The debt servicing component of the budget is the highest cost and adds to the current deficit as well. Significantly the recent build up of the public debt has not been due to developmental expenditure, but the escalating costs of the war. Therefore we are not merely facing inflation due to current unproductive expenditure but reaping the results of past policies. The burden of public debt of massive proportions will continue to exert inflationary pressures in the future. The current massive increase in war expenditure not only fuels current inflation, but fuels inflation of future years. Both the seriousness of the problem and the need to control inflation is recognised by both Central Bank economists and other economic commentators. They also recognise that the efforts of monetary policy to respond and keep in check inflation has tremendous costs on economic growth through the increase in investment costs, as well as the distortion of economic decision making, especially through shifts from productive to speculative enterprises that high rates of inflation induce. Further public expenditure itself is distorted with capital expenditure that is sorely needed being denied. The essential need is to rein in public expenditure by curtailing the expenditure on the war, wasteful administrative costs and unnecessary subsidies. The irony of the situation in the country is that policy makers recognise these facts and issues and have urged for policies in the right direction, but the actions of the government are to no avail. In an article published in the Financial Times not so long ago entitled WHY WORRY ABOUT INFLATION?, W.A Wijewardena Deputy Governor of the Central Bank of Sri Lanka explained the dangers of inflation lucidly. He began the article with the arresting definition that “Inflation, a continuous and steady rise in the general price level, is, by any standard, the public enemy number one. By the same token, hyper-inflation, an increase in the general price level to a very high level within a very short period of time, is a killer, akin to a mass destruction weapon.” He explained further that: “From the point of view of economics, there are usually two declared public enemies; inflation and unemployment. Of the two, inflation ranks higher. This is because inflation hurts everyone alike; bankers, businessmen, workers, consumers and so forth.” He went on to explain the dire consequences of inflation in these words: “First; uncontrolled inflations erode the confidence of people in the domestic currency. As a result, governments lose the control over money and fail to use monetary policy to curb inflation. Second, people move away from long term contracts and would be concerned only about the passing moment. Salaries, earlier paid monthly would become payable first fortnightly, then weekly and daily and finally hourly. It would entail a tremendous cost on the employers to meet the demand for paying salaries every hour. Similarly, all other contracts would also be very short-term contracts. People would not think of the future, but only on the passing moments. This type of short-term behaviour on the part of people would cause the economy concerned to collapse on itself due to a lack of long term commitments. Inflation normally brings in several other irreparable damages to an economy. In the first place, inflation discourages exports, encourages imports and widens the gap between the imports and exports known as the trade gap causing problems for the balance of payments and the exchange rate. If the domestic prices are higher, there is no reason for exporters to sell a product abroad. Similarly, imports are encouraged, because of the lower price in the international markets than the domestic market. This is equivalent to imposing a tax on exports and giving a subsidy to imports. Second; inflation favours borrowers and discourages savers, if interest rates are not adjusted to reflect the going inflation rate. This is because when such adjustment is not made, though the amount of money received by way of interest may be high, its real value is lesser and lesser than before. It is tantamount to the awkward situation where savers pay interest in real terms to borrowers. Thus, inflation contributes to enrich borrowers at the expense of savers. The high borrowings so encouraged would further fuel inflation. At the same time, the much needed savings flow would dry up retarding the long term development. Third; arising from the same unadjusted interest rates, inflation discourages financial savings and encourages non-productive types of investments in real estate, gold, bullion and other types of precious metals. Bank deposits, stocks and shares are the main casualties, because their real value falls every year due to inflation. But, on the other hand, real estate and precious metals appreciate in value due to inflation. Hence, as an insulating measure against inflation, people would transfer their financial savings into such non-productive types of investments. But, for sustainable long term growth, the necessity is for savings in the form of financial savings and inflation would dry up that savings flow. Fourth; inflation distorts the resource allocation function of an economy. For the market system to allocate resources among competing uses, a price expressed in terms of another price called the relative price, should change. For instance, if the price of carrots increases relative to the price of cabbages, carrots would become more profitable than cabbages…... But, when an economy is hit by inflation, all the prices would rise simultaneously, so both carrots and cabbages seem to be equally profitable. This would confuse the producers who would now be unable to make any choice between the two products…. Fifth; continued inflation distorts the balance sheets of companies, especially the balance sheets of financial institutions. Companies may record profits in nominal terms, but a large part of such profits are eroded in real terms by inflation. When profits are adjusted for inflation, companies would find that their performance has not been spectacular as has been depicted by the amount of rupees they have earned. In fact, their real position has pushed them backward to a lower level. Sixth; inflation very forcefully hits the vulnerable groups with a weaker bargaining power. Such categories include housewives, students, pensioners and workers whose salaries are not linked to inflation. It would lead to continuous agitation by these grups creating social and political dissension. The country, instead of using its resources for investing in long term growth generating projects, would have to spend its energy and resources for solving such social issues.” He concluded, “Thus, inflation is the unrivalled public enemy number one.” This is indeed a very comprehensive account of the dangers of inflation especially on long term growth. What better analysis of the serious consequences of inflation is needed? What is needed is a resolve on the part of the government to bring into alignment its expenditure with revenue. A budget deficit is not necessarily bad. It must however be contained within manageable proportions. Most important is why and for what purposes the deficit is incurred. Unfortunately, the Sri Lankan situation is one where it is too large and the finances are used for “unproductive” purposes. When the burden of the resultant inflation is passed on to the monetary authorities, the job is likely to be ill done as the impact of tight monetary policies have adverse impacts on production and growth and sometimes is itself a cause for further inflation by raising costs of credit and the distortion of investment from productive purposes to speculative. The bottom line is that there is no way that inflation could be controlled without fiscal discipline. It is for this reason that some countries have imposed mandatory requirements such as a constitutional provision that a Minister of Finance and Governor of the Central Bank has to resign when inflation goes beyond a certain level. No such accountability is ingrained in our system. Consequently the real costs of inflation are passed on to future governments and future generations. In India, there is a view that inflation beyond 5 percent is unsustainable politically with incumbent governments losing elections. Do we have this political safety valve? Time will tell. |

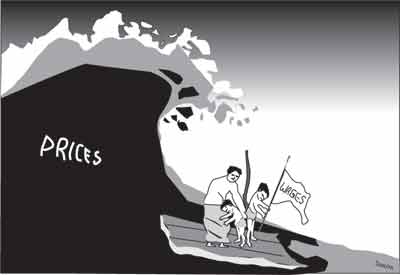

Inflation is deemed to be the most serious economic problem facing the country and the one that appears to be most intractable at present. Inflation continues to be at a double digit level, fluctuating between 12 to 20 percent. In actual fact inflation is a symptom of deep seated imbalances in the economy. External factors, the most notable being that of the rise in fuel import costs have also been responsible for the spiralling inflation. Some of the causes of the current inflation have roots in the economic policies of the past.

Inflation is deemed to be the most serious economic problem facing the country and the one that appears to be most intractable at present. Inflation continues to be at a double digit level, fluctuating between 12 to 20 percent. In actual fact inflation is a symptom of deep seated imbalances in the economy. External factors, the most notable being that of the rise in fuel import costs have also been responsible for the spiralling inflation. Some of the causes of the current inflation have roots in the economic policies of the past. || Front

Page | News | Editorial | Columns | Sports | Plus | Financial

Times | International | Mirror | TV

Times | Funday

Times || |

| |

Copyright

2007 Wijeya

Newspapers Ltd.Colombo. Sri Lanka. |